Watered down

Penn bid would be dilutive unless it monetizes Flutter stake, say analysts

Flutter stake could hold key for any Boyd bid for Penn.

In +More: The CMA throws in big hurdles for Spreadex.

Shares week sees more negatives than positives.

By the numbers: state-by-state tax takes in the year-to-date.

There's only good in leaving with a suitcase full of load.

Hard Rock Bet is all about fun and innovation. With a top ranked sportsbook & casino product, unique access to US states, and a globally recognized brand, join our team to help shape the online experiences that millions love. We’re currently seeking:

And other amazing positions here.

Risk of dilution

The kicker: Any bid from Boyd Gaming for Penn Entertainment would be dilutive for its share price, unless it was paid for in cash and/or if any joint bid with Flutter involved the monetization or other “surfacing of value” for its 5% stake in the US online leader.

Watering down: Such is the view of the analysts at Morgan Stanley, who have warned that Boyd Gaming should be wary of pursuing a “dilutive” bid for rival Penn Entertainment “for the sake of growth.”

The team suggested almost all scenarios involving a cash and equity offer would harm Boyd’s prospects in the key areas of capital return, balance sheet and downside protection.

MS argued that the chatter this summer over the potential for a bid for its rival casino operator “put near-term pressure” on the Boyd share price.

Tag team: Yet, among the “credible” bid rumors from this summer was the potential for Boyd to team up with Flutter, with which it currently has a long-term market access agreement as well as a 5% stake.

As Morgan Stanley noted, to date Boyd has always viewed its 5% stake in FanDuel – currently worth ~$1.4bn or ~25% of its own market cap – as “strategic.”

But the team added that “any monetization of the stake or other surfacing of value” could act as a potential positive catalyst for the share price.

Mind the gap: In upgrading Boyd to an Overweight rating, the MS analysts said its current valuation discount to the rest of the sector was “staggering,” given it still owns ~90% of its real estate (vs. the opco/propco models of most of its peers) and the Flutter shareholding.

Meanwhile, having returned ~25% of capital to shareholders via buybacks, the team suggested Boyd’s “commitment” to returning capital was also attractive.

At the same time, the regional casino business should see a stabilization after several quarters of declines.

Sticky situation

It’s too late, baby, now it’s too late: The Boyd upgrade came in a sector note, which suggested the gaming sector has been “stuck” in the last two years amid sluggish fundamental, high and rising interest rates and “late cycle” economic concerns.

By comparison the S&P – helped by the performance of the Mag 7 – has reached new highs, leaving the widest valuation discrepancy vs. gaming in years.

That was then: The team noted current concerns that weaker discretionary spending means there are renewed fears over a hard landing in the US. Gaming was previously seen as being recession proof – that is, until the financial crisis in 2008 when casino visitation and spend/visit declined in all markets.

At that time, the big casino operators were knee-deep in financial leverage.

Now, however, most of the largest groups have swapped financial debt for rent with most going down the opco/propco route.

This change in the business model “could mean downside is exacerbated by higher operating leverage compared to history,” the team surmised.

Venture capital firm Yolo Investments manages in excess of €500m in capital across 100 exciting fintech, gaming and blockchain companies. The Yolo Investments' Gaming fund, regulated by the Guernsey Financial Services Commission, has taken positions in fast-growth suppliers and operators, including Dabble and Enteractive. Yolo Investments (yolo.io) wants to hear from readers of this newsletter. Get in touch with your pitch, or for a chat about innovative products which can plug into our investment ecosystem.

+More

Spreadex: Star Sports has expressed an interest in picking up selected elements of the Sporting Index business, where the bid to buy the business from Spreadex is the subject of a Competition and Markets Authority review.

In a response to the CMA, Star said it would be “interested” in pursuing a divestiture that would help correct the substantial loss of competition caused by the original merger plans.

In its own response, Spreadex said it disagreed with the option put forward by the CMA for it to sell some of its own assets.

It prefers the option of selling some of the Sporting Index assets alongside a transitional services agreement with regard to the index technology.

Betsson said it is considering issuance of €100m of new three-year bonds, with the net proceeds being used to pay off an existing bond as well as potential M&A.

Superbet and Huddle have agreed a partnership that will see the integration of the supplier’s SGP, player props and micro-betting markets.

Earnings in brief

Entain: Ahead of investor meetings this week, Entain issued a brief update saying the momentum from Q2 has continued into the current quarter, with online NGR growth ahead of expectations and UK & Ireland returning to YoY growth “earlier than expected.”

Allwyn: Revenue rose 5% YoY to €2.15bn but adj. EBITDA fell by 11% to €340m, though excluding the investment made in the UK National Lottery it was up 4%. The company said it saw strong organic growth in Austria, Czechia, Greece and Cyprus.

CEO Robert Chvátal hailed “another successful quarter in terms of financing” after securing a €450m term loan.

Analyst takes – Light & Wonder

A rising tide: The team at Jefferies said, after meeting with management, they believe earnings momentum is continuing to build, with the analysts suggesting the digital and social gaming segments of the business as key beneficiaries from the B&M progress.

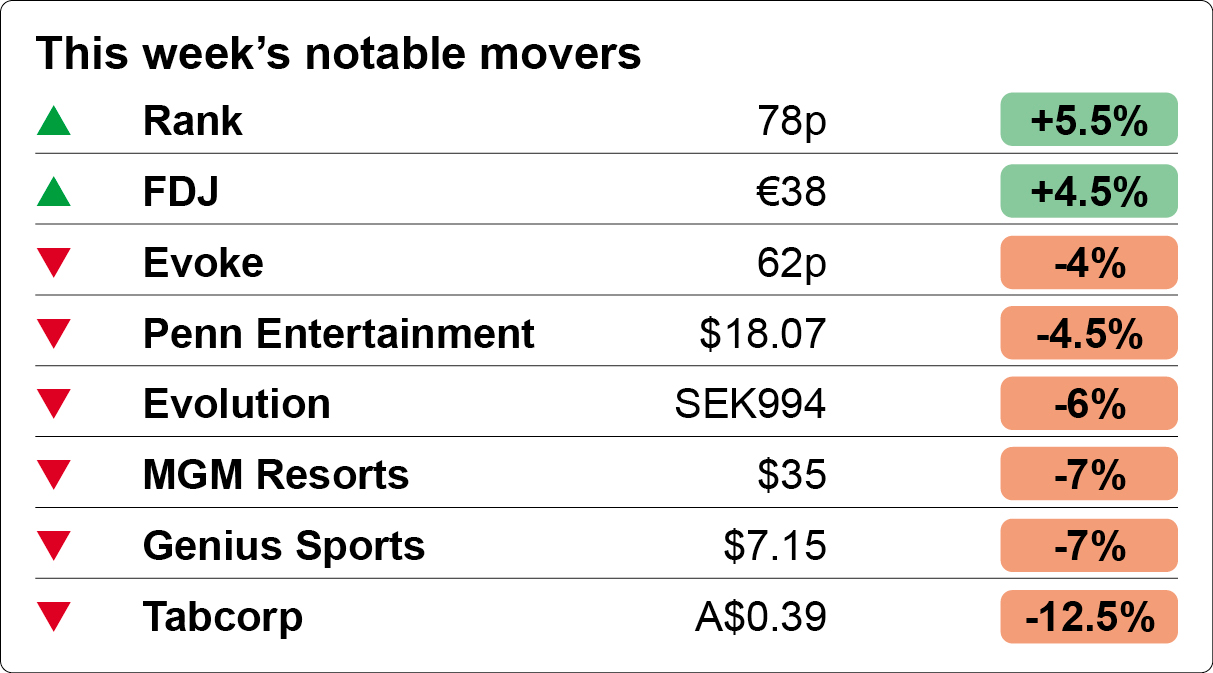

Shares week

Pain, no gain: In a bad week for equities generally, with questions over a hard or soft landing in the US to the fore, the sector managed only small gains on the week, with Rank enjoying a 5.5% uplift helped by a note from Peel Hunt.

Tabcorp was the worst performer for the week, failing to recover any ground with investors after announcing it would not meet its 2025 targets and reporting an impairment charge that led to a A$1.36bn ($907m) after tax loss.

The worst performer of the sector’s top eight stocks was MGM Resorts, down 7% after a negative response to the July data from Las Vegas.

Evolution shipped 6% this week, while Galaxy was down close to 5% and Churchill Downs fell nearly 2% on the week.

Aristocrat was near enough static, but Las Vegas Sands was up 2% as was DraftKings, while Flutter was up over 1%.

Fallen idols: The out-of-favor UK-listed Entain and Evoke continue to languish. Entain, up less than 1% last week, and Evoke, down nearly 4%, continued to trade well below their highs for the year.

In fact, analysis from Citizens showed each is currently trading at around 50% of the levels of their respective 12-month highs.

Kero is a premier micro-betting provider, powering more than 150 operators across the globe.

Our extensive coverage of fast markets in Football, Basketball, Baseball, and Soccer is a proven method for increasing in-play handle and hold.

Talk to us about how we utilize algorithmic recommendation to power highly contextual micro markets for the ultimate in-play experience.

By the numbers

New York: Sports-betting GGR was up 27% to $125m on handle that was up 29% to $1.44bn. FanDuel remained the market leader on 42%, down slightly YoY, while DraftKings kept up with the pace on 32%.

Marginal gains: The team at Jefferies pointed out that FanDuel maintained its lead on margins with 10.3% hold vs. 8.2% for DraftKings and 5.5% for BetMGM.

Ohio: Sports-betting GGR rose 48% YoY in July to $55.1m on handle that was up 44% to $476m. FanDuel led with 38% of GGR, followed by DraftKings on 32%.

Analysts at EKG noted recently the success being enjoyed in Ohio by bet365, which achieved 11% share.

The team at Jefferies also noted it gained a 12% GGR share in Kentucky, which, as the analysts pointed out, was more than BetMGM, Caesars and ESPN Bet combined.

Arizona: The June data is finally in and showing GGR up 94% YoY to $31.6m. FanDuel led with 44%, followed by DraftKings on 34%.

Colorado: Sports-betting GGR was up 31% in July to $32.5m on handle that rose 14% to $320m.

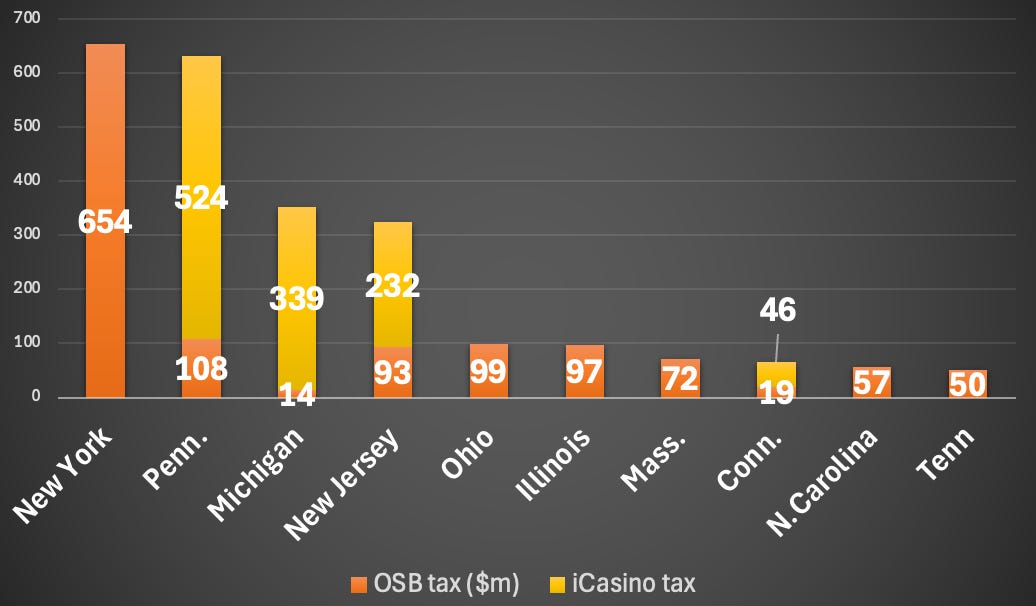

Taxing situation

Eye opener: Two posts on X from Alfonso Straffon, ex-Deutsche Bank analyst, displaying the YTD taxes paid by operators on OSB and iCasino elicited a variety of responses, but primarily the extent to which New York and Pennsylvania lawmakers are likely happy with their decisions on tax rates.

New York’s 51% tax rate on OSB means that by virtue of the state’s size and importance to key operators it tops the table in terms of OSB tax take by a wide margin.

But the extent to which it is leaving money on the table by not licensing iCasino is clear from the position of Pennsylvania.

The Keystone State racked up a combined $632m, with iCasino worth $524m of taxes – and, as Straffon pointed out, unlike New York that total does not include the numbers for August, suggesting it will lead the table when the state reports likely this coming week.

Where’s my cut? Michigan is perhaps the most curious state within the top 10, with a total of $353m almost wholly coming from iCasino taxes while OSB generated a mere $14m.

Here, the lawmakers might well be questioning the wisdom of allowing for promotional deductions, which means the effective tax rate is just 3.4%.

Like, totally: Overall, Straffon noted the blended tax rate for iCasino in the YTD stands at ~25% while for OSB it is at 21%. Across the 34 states tallied the total tax take in the YTD stands at ~$2.8bn, with 42% coming from iCasino and 58% from OSB.

🤫 Top 10 sports betting and iCasino tax takes 2024 YTD

Getting to $33bn

Paper lion: The team at JMP broke down their estimate for handle on the just kicked off football season by month. Between August and February, they estimate $33bn will be wagered across the whole season with the peak in September and October, when they suggested operators will share $14bn of handle.

That is also when football as a percentage of total handle will peak at around 65% before tailing off as NBA and NHL return in Q4.

🏈 All kicking off

Our new, multi-tenant platform is off to an auspicious start…

Live for over 100 flawless days:

Out of soft launch in <2 weeks across 2 sportsbooks

0% downtime across multiple releases and major events

0 rollbacks across major product releases

Anyone that has endured a maiden platform launch can attest to just how significant that is.

We’ve built a powerful new tool for the industry, and we're looking to collaborate and grow alongside our partners, deploying our cutting-edge tech to launch unique and engaging new products.

Get in touch to find out more.

Calendar

Sep 25: Flutter investor day

Oct 17: Entain

Oct 24: Betsson, Evolution

Oct 25: Kindred

An +More Media publication.

For sponsorship inquiries email scott@andmore.media.