The stragglers: a look at the losers in New Jersey

New Jersey analysis, Evolution’s Asia factor, Q1 promo analysis +More

A look at the operators bringing up the rear in New Jersey.

DraftKings vs. Fanatics in the Garden State.

The growing importance of Asia in Evolution’s revenues

Is there any sign of a Q1 promo slowdown in the US?

Just another candle chasing a spark.

Bringing up the rear

Granular fever: As the longest-standing petri dish of US sports betting and iCasino, it was a boon to market observers to be given a more granular dataset by the New Jersey Division of Gaming Enforcement for March.

For the first time, we could be sure which operators had produced what proportion of the GGR under any given skin.

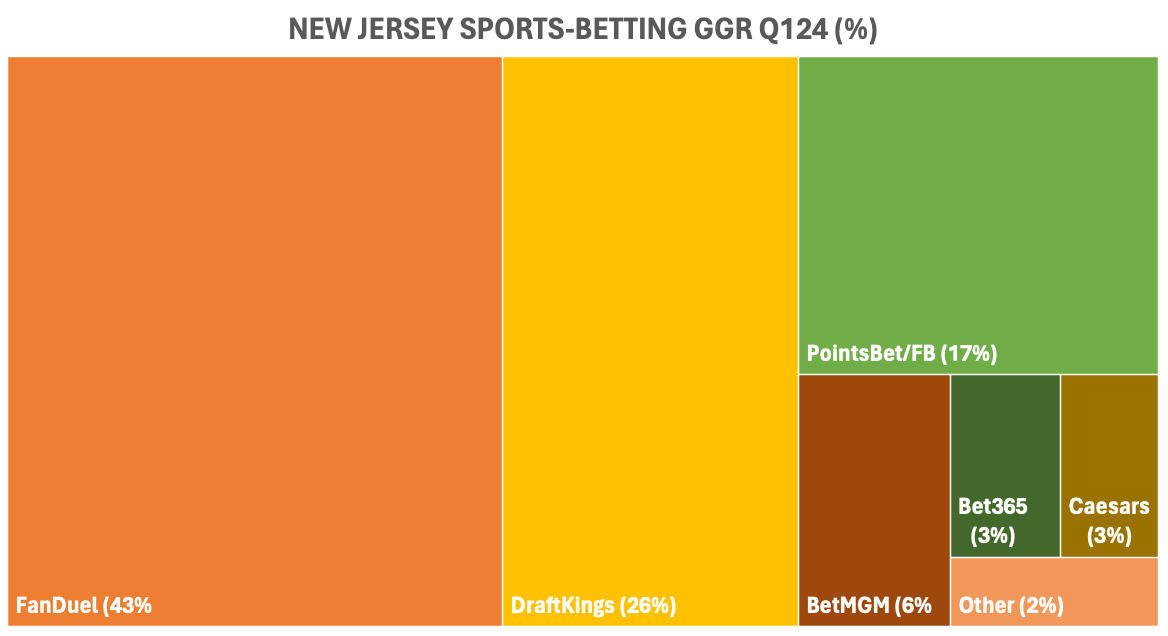

Three’s company too: As a recap, the new data presentation from New Jersey only confirmed what we already knew about the top of the market, namely the dominance of FanDuel and DraftKings, at least throughout Q1.

As was pointed out by EKG, the picture shifted in March with DraftKings finding itself under pressure from Fanatics.

It grabbed the second spot with a GGR of $20.1m vs. the $17.6m for DraftKings, a move that EKG ascribed to Fanatics stealing some VIP business from its rival. See ‘DraftKings vs. Fanatics – NJ edition’ below.

🥧 GGR in New Jersey in Q1 by operator

Venture capital firm Yolo Investments manages in excess of €500m in capital across 100 exciting fintech, gaming and blockchain companies. The Yolo Investments' Gaming fund, regulated by the Guernsey Financial Services Commission, has taken positions in fast-growth suppliers and operators, including Dabble and Enteractive. Yolo Investments (yolo.io) wants to hear from readers of this newsletter. Get in touch with your pitch, or for a chat about innovative products which can plug into our investment ecosystem.

Breaking down the others

Wheat and chaff: While the data confirmed what we knew – i.e. FanDuel and DraftKings’ market leadership – it also more clearly defined how badly the losers are performing lower down the ladder.

Sporttrade: The first of the betting exchanges in New Jersey, which operates under a skin from Bally’s Atlantic City, is clearly struggling to expand beyond an initial toehold. In March, Sporttrade generated a negative GGR of $188k, which wiped out its accumulated gains from the first two months of the year of $168k and left it $20k in the hole.

Betway: Listed parent company Super Group put its US operations under a strategic review in early March, and the New Jersey data indicates just why it is considering its options. The OSB operation made a GGR loss of $115k in March, which more than swallowed up the gain of $108k in the first two months of the year and left it nursing a Q1 loss of slightly more than $7k.

In iCasino, Betway doesn’t fare much better with revenues in March coming to $199k, bringing Q1 GGR to $728k.

Unibet: Kindred has, of course, just this month pulled the plug on its New Jersey operation and it feels akin to kicking an old dog to point to its performance in Q1, but still… The business managed a GGR profit of $79k in March and a $266k positive outcome for Q1.

iCasino was slightly better at $160k in March and $928k for Q1. It is at least in positive territory but the business was clearly nowhere near where it needed to be to be kept alive.

Prophet Exchange: The second P2P betting exchange is, in truth, faring no better than rival Sporttrade. Its GGR for March stood at $81k, which at least means it was able to recover from the $35k of losses in January and February, leaving it with a positive Q1 GGR total of $46k.

Tipico: A look at Tipico’s numbers perhaps explains why it is thought to be on the verge of selling its US sportsbook backend and presumably shutting up shop in the US altogether. In March, the operation in New Jersey managed a GGR of $292k, which added to the $826k from the first two months of 2024, leaves it with a positive GGR of $1.1m.

In iCasino, things look slightly brighter with March revenues of $1.3m while Q1 stood at $3.48m.

Prime: It is far too early to pronounce on Prime Sportsbook’s likely impact in New Jersey after it only got the OK to launch at the tail end of March. All eyes will be on the numbers for the next few months to see how it fares in only its second state after Ohio.

BetParx: With a footprint in Pennsylvania, Michigan, Ohio and Maryland alongside New Jersey, it might sound harsh to suggest this is one of the stragglers. However, the sports-betting data shows it’s barely keeping its head above water in the Garden State with a positive GGR of $232k in March and a Q1 total of $627k.

Similarly to Tipico, the picture for betParx is more positive in iCasino where March GGR stood at $1.29m, leaving the Q1 total at $3.3m.

SuperBook: The Las Vegas-based SuperBook has been in operation in New Jersey since August 2021, hoping to target the ‘sharp’ audience, but it is yet to make much of an impression. GGR in March amounted to $131k, helping to make up for the minor $9k loss in January and February and leaving it a Q1 total of $121k.

Tier 2 challengers

Aside from the actual Tier 2 or BetMGM, Caesars and now Fanatics, several brands are pushing to establish a position behind the leaders.

Hard Rock Bet: Having only launched in August, Hard Rock is still in the early stages not only in New Jersey but also nationally. As such, the poor March outcome with a GGR of only $7k is merely a blip even just in terms of the quarterly GGR of $1.5m.

ESPN Bet: Also clearly in the early days of a national push, ESPN Bet only appears among the others due to a poor January and February. In March it generated GGR of $4.3m, leaving it in fifth position.

Bet365: Another in the camp of ‘definitely not leaving’ is bet365. It also embarked on a multi-state challenge in the US, yet may be hoping to improve the outcome in New Jersey where revenue in March came in at $3.1m, bringing Q1 to $9.8m. Add in iCasino GGR in March of $1.3m and a Q1 total of $3.5m.

iCasino only

There are also several iCasino-only operators where the calculations over the worth of New Jersey will be different without the costs associated with running a sportsbook.

These include Bally’s, which generated GGR of $6.3m in March and $17.8m in Q1, and the Bally’s-owned Virgin Casino on $1.8m in March and $5.4m in Q1.

Resorts saw GGR hit $1.9m in March and $5.7m in Q1, while Ocean Casino Resort GGR in March came in at $2.5m and $7m in Q1.

Flutter-owned PokerStars saw poker GGR for Q1 hit $2.6m, helping total iCasino GGR come in at $4.3m for the quarter.

The Boyd-owned Pala/Stardust generated $2.4m in Q1.

The recently launched, and soon-to-be DraftKings-owned, Jackpocket recorded $1.9m in Q1.

Mohegan Sun saw GGR hit $2.8m in Q1 and $1.1m in March.

And PlayStar generated $1.8m in March and $4.9m in Q1.

The bottom line

Facing facts: For some of those above, whether to stick it out or follow Kindred/Unibet down the exit path is a question that is likely to become acute over the seasonally slower summer months.

Specifically, many will have to decide whether to hang in there for another football season. At some point, even the most stubborn operators might come to see New Jersey as a bust.

Our top seven sports betting MarTech must-haves

The industry ballooned to a whopping $63.53 billion in 2022. And guess what? It's predicted to grow, with an 11.3% CAGR from 2022 to 2031.

Of course, this digital gold rush has brought about intense competition amongst sports betting companies, and the demand for software that revolutionises and enhances the player experience has soared.

In the sports betting arena, having the right arsenal of tools isn't just helpful — it's the key to success. We've scouted the digital playing field and handpicked seven tech champions that will elevate your game to hall-of-fame status.

See here: https://www.trafficguard.ai/blog/ultimate-tech-stack-for-sports-betting-marketers

DraftKings vs. Fanatics – NJ edition

Boys keep swinging: The team at Jefferies produced a telling graph looking at the DraftKings and Fanatics swingometer in New Jersey in Q1. As can be seen, there have been some significant month-on-month swings, which, as reported previously by EKG, appear to be driven by a small number of VIPs that have switched from DraftKings to Fanatics.

Evolution in Asia

Can’t rely on you: Evolution saw its revenues break through the half-a-billion euros mark in Q1 to €502m, confirming the live casino and games provider’s remarkable ascent to the very top of the iCasino tree.

Little remarked upon by the company during the Q1 call with analysts was the importance of Asia to the business.

The only comment came from CEO Martin Carlesund who said the region continued to be the company’s fastest-growing, coming in 28% up YoY.

East rising: It is indeed a remarkable ascent. In Q1 of 2020, Asia was worth just €20.8m to Evolution or 18% of total revenues of €115m. Four years on, that total has grown to €198m or 39% of total revenues.

It means Asia has eclipsed Europe as the largest region by revenue, which was worth €191m or 38% of total revenues in Q1.

Commenting on the FY numbers back in February, the analysts at Regulus pointed out the Evolution share price effectively suffered from an Asia discount due to the lower quality – read unregulated – nature of the Asian business.

The promo debate

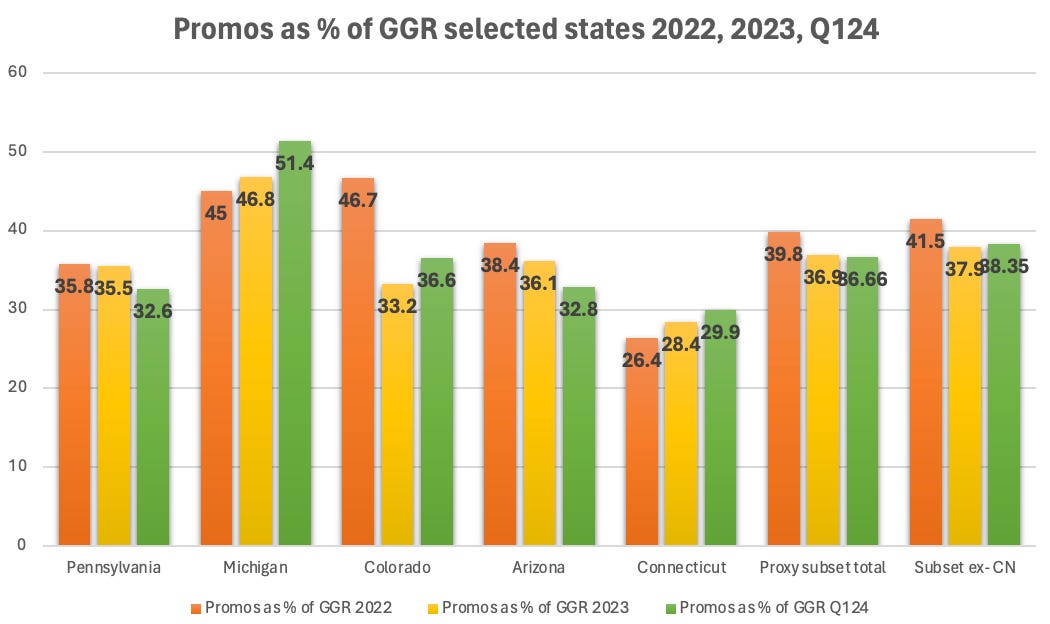

Slice and dice: The extent to which the promotional environment is in any sense becoming less competitive is a hotly debated topic. Adding further insight is a slice of research from Deutsche Bank, which analyzes the data from the select cohort of states that publish promotional data.

The proxy group includes Pennsylvania, Michigan, Colorado, Arizona and Connecticut. It is a fair assumption this group provides a representative sample of what is happening across the market.

Fall guys: The DB team showed how between 2022 and 2023, promotional intensity did drop across the five states from 39.8% of GGR to 36.9%, with the decline largely ascribed to a drop off in Arizona from over 38% to just over 36% and a more substantial fall in Colorado from nearly 47% to just over 33%.

But notably, the promo percentage in the larger markets of Pennsylvania and Michigan was essentially flat.

It is also worth noting that when Connecticut is stripped out – where promo levels are far less than elsewhere due to the market effectively being a straight duopoly of FanDuel and DraftKings – it stood at nearly 38% vs. 37%.

Moreover, for Q124, while the promo percentage for the proxy group as a whole fell marginally on the 2023 number – 36.7% vs. 36.9% – in the proxy group ex-Connecticut the promo percentage rose vs. the 2023 figure.

💵 The promo giveaways continue into Q124

Calendar

Apr 30: Caesars Entertainment, Lottomatica, Melco Resorts

May 1: MGM Resorts, Bally’s, Rush Street

May 2: Penn Entertainment, VICI, DraftKings (earnings)

May 3: DraftKings (call)

Let’s Get Results. InclineBet’s specialist digital marketing services, including high-performance UA, CRM, Creative and Branding for clients in global regulated markets, are backed by data analytics and measurable results. With our deep market focus and unrivaled expertise, we build brands and help you acquire high-value customers and maximize lifetime value.

We give you a competitive advantage. Learn more. incline.bet

An +More Media publication.

For sponsorship inquiries email scott@andmore.media.