Tarnished

DraftKings’ attempt to rewrite the OSB rules backfires

Analysts ponder potential brand damage following surcharge climbdown.

Bet365 to be named as the first-ever gambling Champions League sponsor.

A revival in UK-listed sector fortunes in the shares week.

By the numbers: the issues caused by Evoke’s long-term debt.

And his coat is torn and frayed, it's seen much better days.

Hard Rock Bet is all about fun and innovation. With a top ranked sportsbook & casino product, unique access to US states, and a globally recognized brand, join our team to help shape the online experiences that millions love. We’re currently seeking:

And other amazing positions here.

Losing its shine

A supposedly fun thing I'll never do again: DraftKings’ decision to call a halt to its planned player surcharge at least had the benefit of being swift. Having initially floated the plan with its Q2 earnings announcement on August 1, it was pulled just 13 days later.

Analysts at Truist pointed out DraftKings clearly believed others would “come to the same conclusion” that surcharges were the best measure to counter higher taxes.

“That hasn’t been the case,” the team noted.

Timeline to a climbdown

Aug 1: DraftKings announces a plan to institute a “nominal” player surcharge in high-tax states. The next day CEO Jason Robins tells Sportico the “vast majority” of customers would “not be very sensitive” to the new surcharge.

Aug 5: Rush Street Interactive is the first company to come out publicly and say it would not be following suit.

Aug 7-8: On earnings call, Entain interim CEO Stella David says BetMGM was “observing with interest.” while Penn CEO Jay Snowden says the DraftKings move was “unexpected” but “definitely interesting.”

Aug 13: On its Q2 call, Flutter CEO Peter Jackson says it has “no plans to introduce a surcharge on winners.”

Aug 13: Within the hour, DraftKings issues a statement via X that “after hearing feedback” from customers it has decided not to proceed with the surcharge after all.

Aftershocks: The team at Wells Fargo expressed surprise at “how quickly DraftKings pivoted” but they argued the ramifications might last a lot longer.

In terms of potential fallout, the team speculated DraftKings might have to do the equivalent of an “apology tour,” handing out more promos.

It won’t have been helped by the erroneous golfing email snafu last week.

The company could also face more investor skepticism regarding its betting lines.

Regulatory backlash: The customer reaction might not be the only fire left to fight. EKG suggested the potential backlash might extend to state regulators, who “would not have looked kindly on any attempts to skirt paying taxes.”

Along similar lines, Jefferies said the original news had awakened fears among investors of DraftKings making a tactical error.

Taking such an adverse posture at what remains an early stage in the development of regulated online activity might hurt further lobbying efforts to pass iCasino legislation.

Is this a test? It was, in fact, the latest misstep in what Wells Frago characterized as a “tough” past two or three months.

This includes the original news from Illinois of increased taxes, the higher customer acquisition costs as revealed in the Q2 statement and the cut to 2024 guidance.

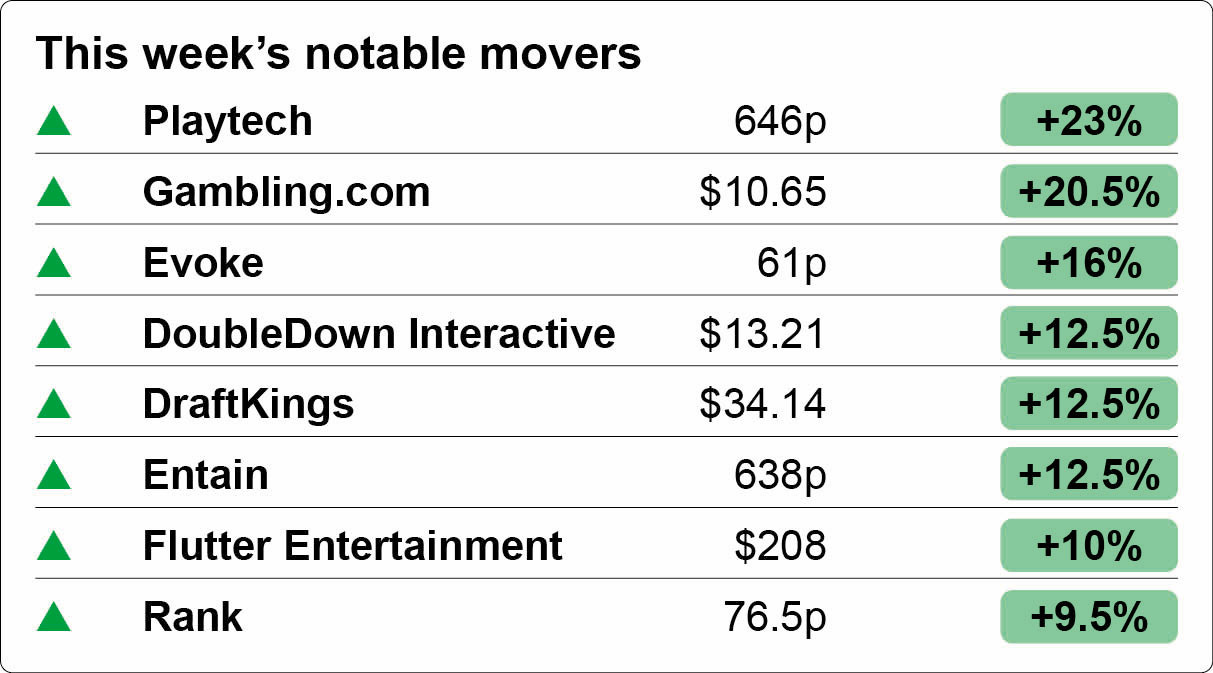

Relief rally: In the short term, the decision to call a halt was welcomed positively by investors. Helped by the wider market bounce towards the end of the week, DraftKings’s shares were up 12.5% in the days following the reversal.

Venture capital firm Yolo Investments manages in excess of €500m in capital across 100 exciting fintech, gaming and blockchain companies. The Yolo Investments' Gaming fund, regulated by the Guernsey Financial Services Commission, has taken positions in fast-growth suppliers and operators, including Dabble and Enteractive. Yolo Investments (yolo.io) wants to hear from readers of this newsletter. Get in touch with your pitch, or for a chat about innovative products which can plug into our investment ecosystem.

+More

Betfred US CEO Kresimir Spajic has told EGR that a market exit is “on the table.” Recall, the company has already pulled the plug in Maryland, Ohio and Colorado.

Fanatics has launched in Louisiana, its 22nd sports-betting state, via a market access deal with Penn.

Betway has been announced as the new official betting partner for the EPL’s Nottingham Forest. This follows on from the deal announced ahead of the new season with Manchester City. Meanwhile, Luckia is the new official betting partner for LaLiga in Spain and Mexico. The agreement includes the rights of LaLiga EA Sports and LaLiga Hypermotion.

Stats Perform and the English Football League (EFL) have announced an exclusive multi-year partnership for official international live streaming video rights for licensed sports-betting operators.

FuboTV has gained a preliminary injunction to halt the launch of Venu, the sports streaming service from Fox, Warner Bros. Discovery and Disney (ESPN). Fubo filed the complaint on antitrust grounds. The legal issues have likely pushed the launch until 2025.

On social

The week ahead

The big beast of the gaming affiliate world, Better Collective, reports its numbers late on Wednesday with the call the next morning. The team at Redeye last week trimmed its Q2 revenue and EBITDA estimates to €97m and €29m respectively.

The team noted that the first effects of Google’s new policy on media partnerships should also be visible in the numbers.

Recall, in May, Better Collective suffered a double-digit one-day share price fall after the company warned about the consequences of the move.

Bet365’s UEFA deal

Name on the cup: The Stoke-based sportsbook is set to be officially announced as a sponsor of the UEFA Champions League, the first time a gambling operator has been associated with Europe’s premier club competition.

Spot the ball: Eagle-eyed football supporters may have noticed a new name gracing the perimeter board advertising at Wednesday’s UEFA Super Cup final in Warsaw when bet365 flashed up in rotation during Real Madrid’s 2-0 defeat of Atalanta.

The company joins seven other brands, including Heineken and Mastercard, as global sponsors for the competition.

The final regularly attracts a global television audience of over 400 million, easily surpassing the Super Bowl as the most-watched annual sporting event.

Pick that one out of the net: The deal is estimated to be worth around £50m a year and will run for three seasons from the start of this campaign. Alongside sponsorship features such as perimeter boards and stadium branding, bet365 will also run a new pick six game.

Second string: Earnings+More has also confirmed that Betano is to be announced as a sponsor of the UEFA Europa League and the UEFA Conference League after Bwin declined to exercise an option to extend its three-year sponsorship.

Betano’s relationship with UEFA started when it became a sponsor of the 2024 European Championship in Germany.

Bet365 and UEFA were contacted but declined to comment.

The shares week

Bouncebackability: Memories of the yen carry trade crash are already long gone as the sector rode the coattails of a wider market surge late last week, with green arrows seen almost across the board on Friday.

Anarchy in the UK: Leading the way this week were the handful of UK-listed gambling stocks, which were boosted by M&A chatter and, for Evoke, a show of faith from the CEO.

Rocket from the crypt: Confirmation that Playtech was in exclusive talks with Flutter over a buyout of Snai – with a rumored price tag that might exceed Playtech’s market cap – understandably put a rocket under the share price, which soared 23% this week. Flutter rose 10%.

Evoke’s H1 numbers were nothing to write home about, but following the dictum of putting his money where his mouth is CEO Per Widerström snapped up 900k shares or £495,000-worth.

Target practice: Gambling.com pleased its investors with a better-than-expected performance in Q2 and was rewarded with a 20%+ leap last week. The analysts at Jefferies said the beat and raise gives onlookers confidence in the company’s long-term target of $100m in adj. EBITDA.

Algosport are regarded as one of the ‘best-kept secrets’ in the gambling industry, currently supporting hundreds of Tier 1 and challenger operators with our proprietary Algosport Blackbox – a powerful engine capable of supercharging your sportsbook.

We are best known for our next generation Bet Builder/Same Game Multiples product that offers the widest range of sports with unrivalled coverage, markets and features, both pre-match and in-play.

To understand how we could help create more revenue get in touch at www.algosport.co.uk

By the numbers – Evoke debt

Pile driver: Staying with Evoke, the worst is over as far as it being overwhelmed by its debt pile but, as last week’s earnings presentation made clear, the company is still hemmed in by its £1.76bn of borrowings.

CFO Sean Wilkins noted the predicted fall in adj. EBITDA to the end of June meant leverage increased from 5.6x to 6.4x.

“We expect this increase in leverage to be temporary and expect leverage at the end of 2024 to be much closer to where we began the year,” he told the analysts.

The plans for 2026 is a “rapid deleveraging” to below the 3.5x target.

💷 Evoke’s wall of worry

Austerity chic: Notably, Wilkins said one of his “key learnings” in his first six months in the job is the company still has “loads to go on the cost side,” with a “wide range” of manual processes, duplication and inefficiencies to be eliminated.

As much as the company spoke last week about “investing” in its capabilities, it's clear more cuts will be a part of that transformation.

“This ongoing work will lead to a structurally lower cost base, with further annualization impact into 2025, giving us confidence in our 2025 plans,” Wilkins promised.

New Jersey July

VIP MIA: The latest data from Jew Jersey confirmed that Fanatics’ (presumably) VIP-led bounce earlier this year is well and truly over. Recall, it dramatically took second spot from DraftKings in March and April with $20m and $30m of GGR respectively.

But the reversion to the mean has been brutal in the subsequent three months, with the company generating $1.8m in May and June and $2.7m in July.

Sports-betting GGR in July was up 31% YoY to $80m. FanDuel, meanwhile, continued to lead with 41% GGR share, followed by DarftKings on 33%, BetMGM (8%) and Caesars (4%). ESPN Bet maintained a minimal footprint with 3% share.

iCasino GGR rose again, up 26% to $195m. DraftKings led with 26%, followed by BetMGM on 22.5%, FanDuel (19%) and Caesars (9%).

New York: OSB GGR in July was up 33% to $140m on handle that rose 31% to $1.2bn. FanDuel led on 42%, followed by DraftKings (34%), Caesars (8%) and Fanatics (6%).

Maryland: Sports-betting GGR jumped 89% to $41.7m in July, with FanDuel grabbing more than half of total revenue on 51%, followed by DraftKings on 29% and BetMGM on 8.5%. Handle rose 35% to $333m.

Indiana: B&M gaming saw GGR come in at $206m, down 3% YoY. Sports-betting GGR rose 25% to $29m.

Belgium: Total GGR for 2023 was up 17% to €1.7bn despite the restrictions on gambling ads that came into effect mid-year. iCasino revenues rose 20% to €455m while B&M casinos rose 14% to €140m. OSB GGR rose 13% to €238m with retail setting up 2% to €152m.

Join 100s of operators automating their trading with OpticOdds.

Real-time data. Proven trading tools. Built by experts. Meet us at SBC Lisbon & G2E Vegas. Join top operators at www.opticodds.com.

Calendar

Aug 21: Better Collective (earnings)

Aug 22: Better Collective (call)

Aug 28: Gaming Innovation Group

Aug 29: Rivalry

Sep 6: Allwyn

Sep 25: Flutter investor day

An +More Media publication.

For sponsorship inquiries email scott@andmore.media.