Sep 30: Weekend Edition #66

Scandi analyst initiation, XL Media H1, Aristocrat/Roxor, XPoint fundraise, Macau analyst update, Nevada data +More

Thought bubble

Bored with selling Gamesys for the umpteenth time, ex-founder Noel Hayden appears to have embarked upon a tidying up process with his other interests in the betting and gaming space. In early September, his LiveScore business saw a major investment from the Switzerland-based media group Ringier while this week he sold Roxor Gaming to Aristocrat. At the risk of over-interpreting, it appears that one of the European industry’s most significant founders is cashing in at least some of his chips. That feels significant.

Scandi analyst update

Initiating on Evolution, Kambi and Kindred, the team at Jefferies says they present a mixed bag.

Cheap at the price: Looking at the prospects for the biggest names in the Scandinavian listed arena, the team at Jefferies suggests the two B2B providers Evolution and Kambi are underpriced versus the potential for the live casino and OSB opportunities.

For Kindred, however, the analysts contend the company stock will continue to be weighed down by the messy Netherlands situation and tough comps will persist for some time to come.

Evolution

Live forever: Jefferies points to live casino as being the fastest-growing segment in gambling right now and suggests Evolution’s leadership position in providing a “differentiated, complex product delivered at scale” means it is in the “sweet spot” of the gambling sector.

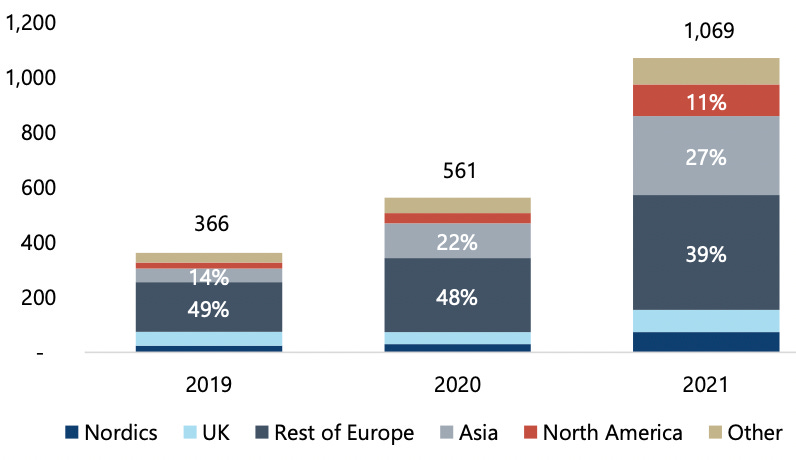

Still, the team did note the bear case for Evolution, including unregulated market exposure (27% Asia, for instance), the Buy consensus on the shares and “flattening” EBITDA margin.

However, “confronted” with substantial cash-flow generation, a scalable platform and the growing global market, they opted to go with the crowd and issue their own Buy on the stock.

Assuming Evolution grows in line with the wider live casino market and maintains its current market share, Jefferies sees ~70% upside to the current share price levels.

💶Evolution’s revenues by geography 2019-2021

Sou

Source: Jefferies

Kambi

Scarcity value: Jefferies says Kambi’s prospects should be helped by positive regulatory changes in the US, where it currently holds a 20% share. It adds that following the loss of the DraftKings contract, “material” new contracts have endorsed the proof of concept while earnings are progressing from existing licensees.

Crucial to Kambi’s prospects, of course, is new jurisdictional licensing and Jefferies argues it is well-placed to benefit from an easier rollout of OSB compared to iCasino.

“Kambi is positioned in the higher growth online sports betting segment where positive regulatory change is driving growth,” the team adds.

Kindred

Dubbele problemen: Jefferies points out that Kindred’s Netherlands troubles occurred at a particularly inopportune time given it was already facing tough comparatives from trading in the pandemic period.

It adds that the risk is Kindred takes time to re-establish itself in the Dutch market while also continuing to run up against tough comps for the next few quarters.

Jefferies notes, though, that there is the potential for corporate action with activist investor Corvex – which has “expressed a desire” for Kindred to consider a sale of the business – now having a seat on the board.

Entain

On the cheap: In a separate note, the Jefferies team have also revisited their Entain thesis and suggests the company has never been cheaper for potential acquirer MGM. The team notes that MGM’s original offer, adjusting for recent currency moves, is now worth ~£16.34.

Paper tiger: Jefferies also notes that 50% of Entain’s shareholders are now US-based. “Those shareholders may welcome an MGM paper offer to ride a digital re-rating,” it adds.

Still, the team has adjusted estimates for Entain lower (EBITDA for FY22 lower by 3%) to reflect tougher trading in H2.

🎯Entain’s share price vs. the implied MGM offer price

** SPONSOR’S MESSAGE** GiG is a leading gaming platform and sportsbook provider for online and land-based operators with digital aspirations. We deliver a full end-to-end solution through our award-winning iGaming and sportsbook solutions. Built for regulated markets and a top-class customer experience, GiG is pioneering the multi-platform era. If you are looking to expand your operations into new, profitable markets, our strategy is the solution.

Find out more at sales@gig.com.

Aristocrat/Roxor Gaming

The Noel Hayden-led UK-based games developer has been bought for an undisclosed sum.

Get your rox off: The deal for Roxor marks Aristocrat’s latest attempt to establish a foothold in the iCasino space after the much bigger aborted $2.8bn takeover of Playtech in February. Roxor was formed in 2019, originally as an in-house developer for Gamesys where Hayden was the majority shareholder.

The sale of Roxor is the latest corporate move following the deal that saw Swiss-based media group Ringier invest £50m for a stake in LiveScore.

Hayden remains a shareholder at Bally, which bought Gamesys for £2bn.

Aristocrat CEO Trevor Croker said in May his company’s M&A ambitions were “transparent” and that he wouldn’t “preclude us from” any deal.

By the numbers: Companies House filings show Roxor Gaming’s turnover nearly doubled to £8.2m in 2021 while operating losses were trimmed by 18% to £17.8m. Roxor games are currently live in New Jersey as well as in the UK.

Streaming M&A

DAZN has acquired fellow sports streamer Eleven Group for an undisclosed sum.

Here come the Belgians: The deal to buy Eleven augments DAZN’s soccer proposition with the rights to the top leagues in Portugal and Belgium, as well as a presence in the markets of Taiwan and southeast Asia, and adds 40,00 games a year to DAZN’s existing soccer portfolio.

Dirty dancing: Eleven is being bought from founder Andrea Radrizzani, owner of EPL side Leeds United. He will take a place on the DAZN board.

Play to the whistle: Included in the deal is Eleven’s sports social media engagement business Team Whistle.

XPoint fundraise

The geolocation startup adds Acies and Bettor Group to its cap table with a “multi-million dollar” funding round.

On point: The new investors join Courtside Ventures, the Raine Group and Suro Capital Sports as the company seeks cash to help drive its expansion in North America. XPoint Verify, its real-money gambling product, is now live in New Jersey and Ontario while its XPoint Lite offering, aimed at DFS operators, is live across the US.

As part of the investment round Bettor’s David VanEgmond will join the XPoint board.

XPoint was formed in 2019 by CEO Marvin Sanderson. Its previous funding round was in February this year when it raised another unspecified amount from Courtside.

Macau analyst update

The news from Macau this week ignites hopes of a return to some form of normality.

Let the good times roll: Prospects for a reopened Macau have been rekindled this week following the eVisa and group visitor news and it has led to the team at Wells Fargo dusting down their Macau recovery scenarios.

The team sees the recent example of Las Vegas’s post-pandemic trajectory as a “decent proxy” for what might happen in Macau.

Recovery position: In the first full year of the full reopening scenario, it suggests GGR could reach ~2.5% above 2019 levels of ~$22.5bn.

Rolling in it: For LVS it could mean medium-term Macau EBITDA of $3.2bn vs. street estimates for 2024 of $2.8bn. Wynn, meanwhile, could see EBITDA recover to $1.07bn vs. 2024 street estimates of $927m.

Underlying assumptions: WF suggests Macau will pace at 50%, rising to 90% of pre-pandemic levels in the first four quarters of recovery. It also assumes mass play per visitor will, like Las Vegas, be at +35% of pre-pandemic levels.

Note: The tourism office says it is expecting the number of visitors during Golden Week to reach up to 25,000 visitors per day.

Earnings in brief

XL Media: Revenues were up 38.2% to $44.5m, while adj. EBITDA rose 60.6% to $10.6m. Over the past year XL Media has shifted away from volume-led casino affiliation in non-regulated European markets to brand-led growth in regulated EU and US jurisdictions, with a focus on sports-betting. CEO David King said he expects the sites to return to growth in 2023, with the focus on “marquee sites” bearing fruit.

STS: Half-year NGR was flat at PLN296m, with 81.6% coming from online and 18.4% from retail, while EBITDA fell 7.1% to PLN117m. In current trading, July and August NGR rose 32% to PLN103m with the return of European soccer.

FL Entertainment: Group revenues for Betclic’s parent company increased 19% YoY to €1.8bn and +15.6% at constant currency rate, while adj. EBITDA was up 16% to €301m. Online sports-betting and gaming revenues were down 3% to €396.6m, while adj. EBITDA was down 4.6% to €103.2m due largely to Bet-at-home being down 16%. Revenues ex-Bet-at-home were up 4%.

Event reviews

iGaming NEXT: Predictions for the future was a big theme in Valletta this week as during the opening panel Todd Haushalter, chief product officer at Evolution, put the questions about where the industry was heading to Tim Heath, founder at Yolo Group, and Robin Reed, ex-founder at GiG.

Heath suggested an exodus might be underway from Curacao given its recent moves to tighten up its regulatory practices. “Some will go to the Isle of Man, some to the Philippines and some to the Pacific island nations,” he predicted.

Reed, meanwhile, suggested that Haushalter’s own company was “building up to do the big one”. Who might that be? He put forward the name Light & Wonder.

Reed also suggested Aristocrat was entering the online space “with a vengeance” (see above). “They are really going to shake up this space in a few years,” he said.

Heard on the floor: Simplebet has enjoyed a good month with the news on its deal for the global supply of micro-betting products to bet365 but, according to talk at the show, there is more news to come with another client in the US soon to be announced. We’re sworn to secrecy, but sources did say Simplebet isn’t resting on its laurels.

East Coast Gaming Congress: Reporting back from the event, the analysts at Truist said there were “strikingly few” worries expressed over the macro picture, despite market turbulence and drops in lower-end customer spend levels

Truist reported Caesars CEO Tom Reeg as saying the post-pandemic operating environment had enabled operators to strengthen their balance sheets and FCF.

Truist said they agreed with the conclusions of an online panel that consolidation was necessary.

Analysts in brief

888: “Catching up” with the newly merged 888/William Hill business, the team at Jefferies noted that high leverage (over 5x net debt/EBITDA) and rising interest rates remained a key concern. Reflecting the current environment, they have cut EBITDA estimates to £394m, noting this is below the £400m threshold that would trigger a £100m deferred payment to Caesars.

GLP: In an initiation note, JMP said the gaming REIT had durable earnings backed by long-term leases and suggested that it could look to further M&A. GLP was recently involved in the sale of the Tropicana in Las Vegas to Bally’s Corporation, which completed this week.

Datalines

Nevada: With August Strip revenues up 5% YoY to $659.7m, the team at Macquarie suggested this supported the thesis of earnings beats for the third quarter. Total Nevada was up 3.5% to $1.21bn. Las Vegas visitation was up 6.4% to 3.2m.

Despite lapping a tough comp, the team at JMP noted 5% growth resulted in the “best August in the history of Las Vegas”.

On the download: Looking at the app data for week 3 of the NFL season, analysts at JMP showed that after a third consecutive week of growth the leaders keep piling on the downloads, with DraftKings leading the way, up 83% YoY on the season-to-date. Total downloads from operators representing 90% of the market were up 19% YoY to 287k.

Uppers: By the same metric, FanDuel was up 34%, Barstool was up 16% and BetMGM was ahead by 13%. However, Caesars was down 4% YoY and PointsBet’s app downloads were down 2% YoY.

Arizona Jul22: Sports-betting GGR was up 43% to $22m on a handle down 8.9% to $290.2m. FanDuel led by GGR with 41.3%, followed by BetMGM (25%) and DraftKings (14%) – this was despite DraftKings being just behind FanDuel by handle.

Oregon Aug22: Sports-betting was up 127.4% at $2.3m, while VLT revenues were down 8.6% to $99.6m.

Newslines

Warning shot: UK bookmaker Betfred has been fined £2.87m by the Gambling Commission for social responsibility and anti-money laundering failures. As a result of those failures it will receive an official warning from the regulator.

Flutter’s Sisal has won the 10-year tender to supply its online sports-betting and gaming platform to Tunisia’s national operator Promosport. The UK group also opened a new FanDuel tech hub in Edinburgh.

Rootz maneuver: The slots operator has received a license in Germany, the 15th license awarded.

GAN’s B2B sports-betting technology and managed trading services GAN Sports debuted in the US, following the launch of GAN Sports with Island View Casino in Gulfport, Mississippi.

What we’re writing

Schrödinger's cat: The latest Pinchpoint went out earlier this week suggesting UK government policy on gambling has now reached the stage of quantum mechanics.

What we’re reading

No country for old men: The Nevada Independent looks at the Fertitta past to understand the future of Red Rock.

Where there’s a hit: BetMGM is sued in New Jersey over software glitches.

On social

Calendar

Oct 4: E+M startup month

Oct 6: E+M podcast

Contact us

Scott Longley scott@clearconcisemedia.com

Jake Pollard jake@openmediaservices.com