Mar 1: Flutter in choppy international waters

Flutter FY, January 22 US OSB estimate, Esports Entertainment Q4, IGT payments unit sale, Rush Street Interactive analyst update, New York analyst update +More

Good morning. On today’s agenda:

Flutter Entertainment talks up the US but struggles internationally.

Esports Entertainment is suffering a cash crunch.

IGT sells an Italian payments unit with the proceeds paying down debt.

Rush Street Interactive gets a positive analyst update.

Flutter full year

Revenues up 37% to £6.04bn, but EBITDA down 6% to £723m.

US revenues up 113% to £1.4bn ($1.9bn).

UK/Ireland adj. EBITDA down 2% to £616m; Australia adj. EBITDA up 37% to £437m; international down 49% to £292m.

FanDuel delivered a first-time positive contribution of $21m in 2021.

Group revenue in the first 7 weeks of the year up 2%.

Ukraine crisis: Flutter noted that “since completing” the merger with The Stars Group it had “materially reduced” its Russian exposure and said the market was worth $41m in contribution in 2021. In comparison, Ukraine was worth £19m.

Peter Jackson CEO: “We have obviously seen an impact in the countries directly impacted. The most important thing for us is our colleagues in and around the region. We’re doing everything we can to support them and their families, including relocation.”

Challenger: Despite owning the leading US sports-betting brand, Jackson said the company was “leaning in '' to the market despite the competitive pressures.

US stats: Sportsbook stakes rose 156% to £11.3bn with sports-betting revenues up 113% to £978m and gaming revenues up 74% to £413m. Total revenue hit £1.39bn with 95% attributable to FanDuel and the rest coming from TVG. Sales and marketing expenses were up 91% to $663m.

Jackson: “We’ve never focused on market share targets. We’re delighted with how the business is performing and pushing really hard. We’re delighted with the market share we have taken and the business has terrific momentum.”

What they said:

Jackson on the stickiness of the US product: “Our customers are voting with their feet, they may take other competitors’ free money but they come back to the FanDuel app.”

Jackson on the benefits for a US listing: “It’s not something we need to do and clearly we are monitoring the markets at the moment and it is something the board will keep under evaluation.”

Jonathan Hill, CFO, on the route to profitability: “We won’t be providing revenue guidance on the US but it will definitely be higher than 2021. In terms of EBITDA, we are not giving specific guidance at this point but it won’t be a significantly bigger EBITDA loss than 2021. We have a clear route to where we are going in 2023.”

Challenging: The international segment is beset by troubles, with tough comparables (on poker in particular) and the disruption caused by regulatory change in the Netherlands and Germany. Excluding all the bad stuff, revenues would have increased 14%. Analysts at Regulus suggest a revival here would depend on the extent to which poker can be revitalized and new markets can be added.

UKI OK: The UK and Ireland segment was hampered in the earlier part of 2021 in particular by continued Covid restrictions on retail trading. Total revenues of £2.06bn were up 2% with sports-betting flat at £1.28bn and gaming revenues of £781m up 5%. UKI online rose 3% to £1.89bn while retail was down 13% to £174m. Online sports-betting was helped by a 25% rise in stakes.

Hill on the UK going forward: “I think the recreational market will remain the better part of the market. But the overall market will probably be flat. We’re just building sustainability now rather than later.”

Further reading: Flutter ties bonuses to responsible gambling metrics.

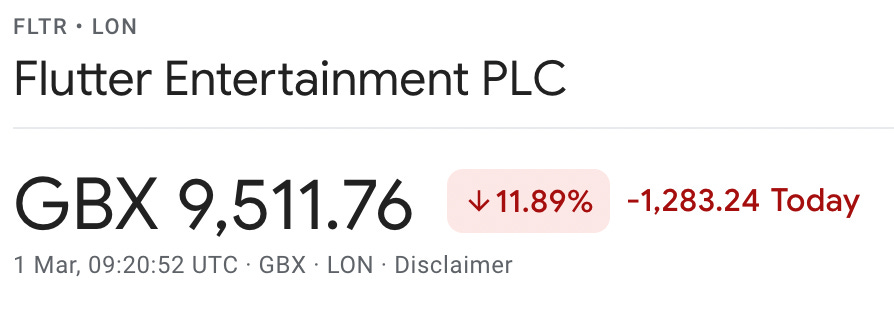

Market reaction: The share price suffered a near 12% fall in early trading on fears over the international business.

** Sponsor’s message: Venture capital firm Yolo Investments is home to €350m of equity in more than 50 of the most exciting companies across fintech, gaming and blockchain. It continues to build one of gaming’s most dynamic portfolios as it eyes up seed and A-stage opportunities across the sector. Its dedicated 28-company, €135m AUM gaming fund already houses holdings in fast-growing suppliers and operators, including Kalamba Games, SimWin and ThriveFantasy. Yolo Investments is also on the lookout for LPs as it looks to scale new concepts, including its high-roller live casino brand, Bombay Club.

As a proud sponsor of Earnings+More from Wagers.com, Yolo Investments wants to hear from readers of this newsletter. Get in touch with your pitch, or for a chat.

BREAKING NEWS: 888 has been hit by a £9.4m fine by the UK Gambling Commission for social responsibility and money-laundering failures. This is the second enforcement action within the past five years after the company had to pay a £7.8m penalty package. UKGB CEO Andrew Rhodes warned that if there was a repeat of the failures, then the Commission would have to “seriously consider the suitability of the operator” as a licensee.

Jan22 US OSB estimate

The New York effect: With only five states yet to report, Deutsche Bank have estimated sports-betting GGR for January will come in at ~$630m, up ~69% sequentially and the same percentage rise YoY. Both metrics were influenced by the New York opening.

Excluding New York, sequential and YoY growth would have come in at 36%. Increase hold accounts for the sequential improvement in like-for-like figures.

Market shares: Looking at the data from Illinois, Indiana, Iowa, Michigan, New Jersey, Pennsylvania and Tennessee for January, DB estimate that FanDuel led the way with 46.7% followed by DraftKings on 20.6% and BetMGM on 16.8%.

Esports Entertainment FYQ2

The owner of the Bethard brand is facing a cash crunch after it missed its Q4 revenue targets and cut its 2022 forecasts late last week.

Out of luck: As with others (Kindred, Betsson et al), Esports Entertainment said the cessation of activities in the Netherlands left a dent in its earnings. Revenue of $14.5m was down 11.4$ sequentially while net losses climbed to $34.5m from a $0.6m loss in FYQ1. The company also slashed its FY22 forecasts to $70m-$75m from $100m previously.

The company also revealed it had only $1m of cash on the balance sheet as of the end of Dec21. Such is the worry that in its 10-K the company said that “certain factors raise substantial doubt about its ability to continue as a going concern” for the next year.

Emergency measures: Analysts at Roth Capital noted with a cash burn of approximately $1.3m a month, the company is resorting to an at-the-money (ATM) program where it can sell shares to raise up to $20m. So far, it has raised over $4m as of mid-Feb. The other looming issue of $35m of convertible notes where the company is currently negotiating “agreeable” terms.

Roth: “Limited transparency in Esports Entertainment’s eventual capital structure makes it difficult to properly value shares and we believe only special situation investors should consider investing in it.”

Cash raise latest: On Sunday, the company announced the pricing of $15m worth of stock and warrants. The offering is expected to close on Wednesday, March 2.

Price crash: Roth cut its target price to $1.40 from $22 prior.

IGT payments unit sale

The €700m sale represents a 17.5x EBITDA multiple.

Deal expected to close in Q322.

Proximity high: IGT has sold its Italian ‘proximity payment’ business LISPAY, previously part of its lottery unit, to PostePay for ~$780m. New IGT CEO Vince Sadusky (appointed Jan22) said the deal was an opportunity to monetize the payments business and also streamline the company’s product offering. The company will use the proceeds to reduce net debt.

Surprise! Truist noted the deal would be a pleasant surprise for most investors who likely were “not even aware” the unit existed.

Zeroing in: Macquarie said this was evidence of Sadusky’s goal of deleveraging and said the sale “further focuses the company’s earning stream on lottery” which now comprise ~80% of EBITDA.

Earnings call: IGT will report its Q421 earnings today, March 1, with the analyst call at 8am ET.

RSI analyst update

Analysts at Roth believe the ~40% downward push on Rush Street Interactive’s shares in January suggests the “take-out expectations have been removed”.

Losing altitude: The Roth team noted the share rose as high as $24 in the summer on widespread speculation that RSI might make an attractive target for possible new entrants such as Fanatics or ESPN. But with uncertainty over the future of other second-tier brands (TwinSpires and WynnBet get a mention), it took the wind out of the M&A talk, at least temporarily.

i of the beholder: But RSI is more than an OSB play, the team adds. “We believe investors are unfairly discounting RSI's iGaming exposure,” the team suggests. “We also believe RSI's iGaming-first strategy offers higher margins over time, where ROIs on CPAs seem lower for OSB.”

Meanwhile, predators are still in the water: “We now believe Fanatics or ESPN are more likely to enter via M&A in 2023, during a period where incumbent leaders are targeting marketing rationalization.”

New York analyst update

Down but not out: Looking at last Friday’s data, Morgan Stanley said the expected fall in handle week-on-week (the first full week after the NFL and also the NBA All-Star game mid-season break) still indicated a run-rate of ~$1.3bn in FY22 GGR, which is above the $1bn forecast.

Morgan Stanley: “It appears excessive promotions partially supported NY's early strength and are starting to see the market show signs of stabilizing as most operators have removed their most generous offers.”

Heavy concentration: Caesars once again saw handle share fall (to 19% from 38% the previous week) with GGR share down at 17% (vs. 48% for Jan) but MS said the latter figure was still ahead of its long-term 10% forecast.

“We maintain our view that market share will be concentrated among the top players and sub-scale operators will find it difficult to compete.”

#StandWithUkraine

Many organizations and individuals involved in the gaming sector have launched a GoFundMe to hello support efforts in Ukraine. Click here if you wish to donate.

See Rasmus Sojmark’s post on LinkedIn for more info on who is supporting the effort.

Newslines

Different meta: Affiliate marketer Playmaker has announced a strategic partnership with MetaBet, a provider of automated and contextual sports betting products.

Ready for the Nether: Aspire Global says it has received regulatory certification for its entire suite of products including sports betting from the Dutch gambling authority. Late last year, Aspire’s PasriPlay division signed a content deal with Holland Casino and in January it signed a deal with Boylesports to supply its yet-to-launch Dutch operation.

Buyback better: Better Collective has initiated a share buyback program of up to €5m to cover future payments relating to “completed and potential new acquisitions”. The group said it was actively pursuing M&A targets and was currently involved in a number of active discussions where shares may be part of the considerations.

Maple syrup: Maple Leaf Sports & Entertainment has named Amazon Web Services its new cloud provider to help develop fan experiences that span augmented reality, virtual reality and sports-betting. MLSE owns the NHL’s Toronto Maple Leafs, NBA’s Toronto Raptors, MLS club Toronto FC and the CFL’s Argonauts.

Calendar

Mar 1: IGT, Playtika Q4, Scientific Games Q1

Mar 2: Rush Street Interactive Q4

Mar 3: Entain Q4, DraftKings investor day

Contact us

Scott Longley scott@clearconcisemedia.com

Jake Pollard jake@openmediaservices.com