Loan sharks

Bally’s Intralot CEO admits to ‘very high’ interest rate on new debt

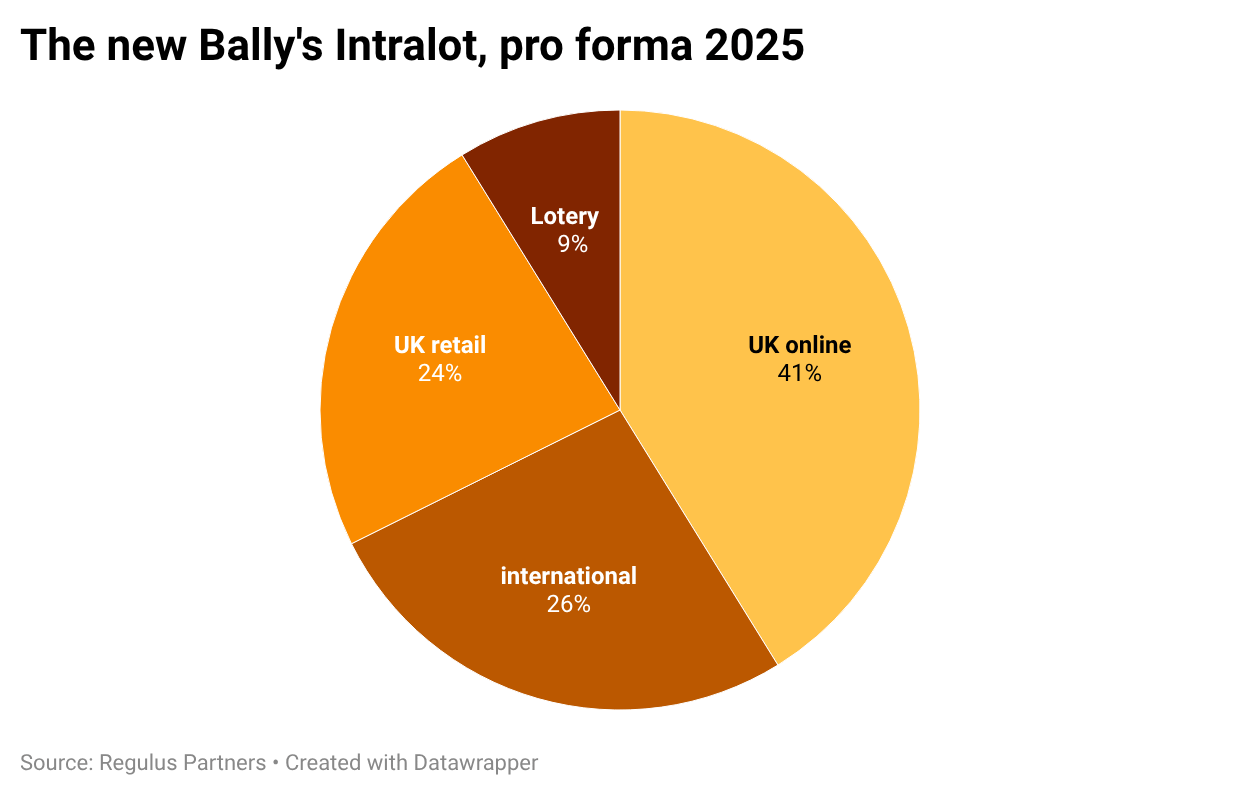

Bally’s Intralot part-funds Evoke buyout with 11% second lien debt.

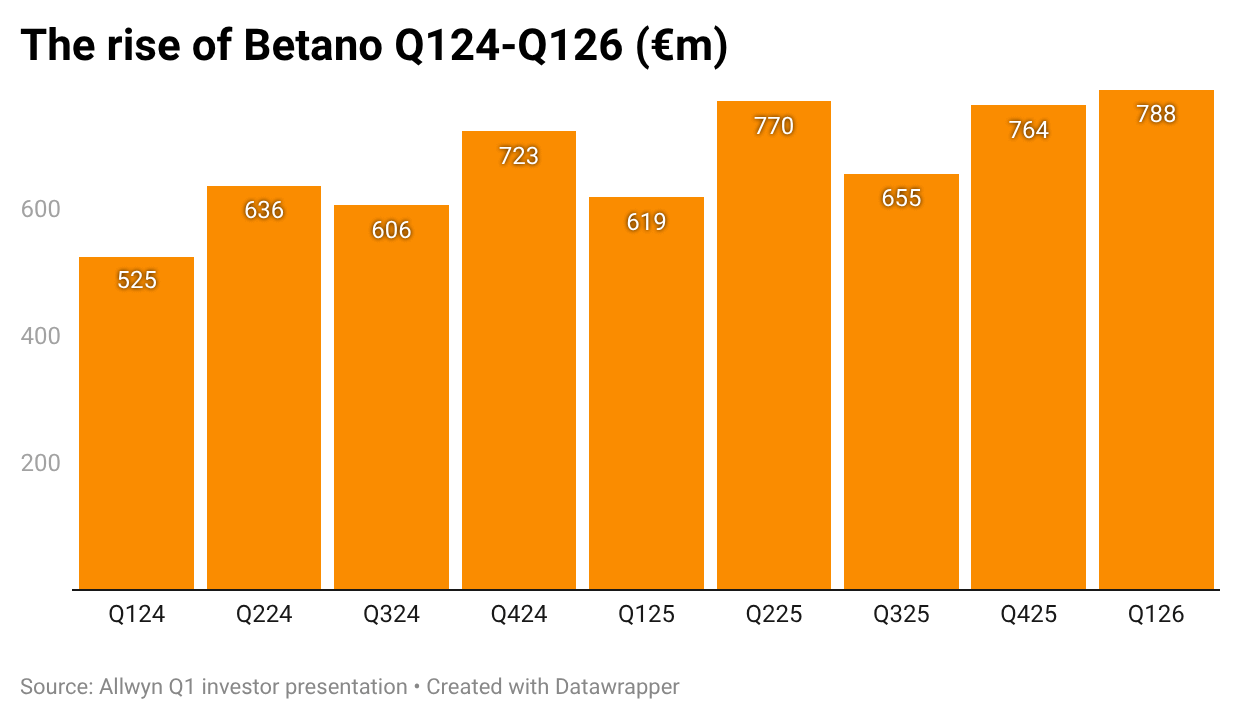

Allwyn discloses Betano’s past two years of growth.

Markets: AGT up as chair resigns, Kjerulf Ainsworth ups stake.

Puts+takes: Macquarie forecasts a bonanza World Cup.

Hard Rock Bet is growing – we know you know! And we want to bring in some more maestros to make beautiful music in our Sportsbook. You need to be among the very best in the industry to be considered for these roles. Are you up to it?

Paying through the nose

Stand together, fall apart: Bally’s intralot CEO Robeson Reeves admitted the company is paying a “very high” interest rate on the £889m newly arranged facility with TPG Credit, Oaktree and OHA used to complete the acquisition of the William Hill and 888 brand owner Evoke.

Reeves was keen to point out that Evoke’s debt, which with the new €889m facility now rises slightly to £1.89bn, is “siloed” from its own €1.49bn of debt.

“What’s really important to understand about this deal, looking at the risk, is that the debt that Evoke has is entirely connected to the Evoke silo,” he emphasized.

“There is no recourse to Bally’s Intralot. Bally’s Intralot shareholders therefore have low downside risk and high upside.”

Jaws of defeat: Regulus Partners said in a note issued late last week that the deal structure just about suits all involved and “probably swerves the risk of bankruptcy,” albeit at the price of dealing with “understandably shark-like” lenders.

“If Evoke underperforms horribly before a turnaround can take place, the debtholders will take ownership,” the team wrote.

“And they can make the biggest problem facing Evoke go away by converting their half of the debt to equity or PIK.”

And you may ask yourself, ‘Well, how did I get here? One of the architects of the merger between William Hill and 888, Vaughan Lewis, writing for his substack late last week, admitted the company was hobbled from the start by its leverage profile.

He wrote that the original transaction structure contemplated approximately £1.5bn of debt and £500m-£600m of equity funding at a time when debt costs were around 4%.

But by completion, after a William Hill license review and subsequent renegotiation, the debt levels increased materially while the cost of debt had more than doubled.

And you may ask yourself, ‘Am I right, am I wrong?’ “A transaction that worked comfortably at 4% interest rates became significantly more challenging at close to 9%,” he said.

And you may say to yourself, ‘My God, what have I done?’ “The strategic logic remained largely unchanged. The economics of the financing did not.”

The turn of the screw: Debt aside, a further factor in Evoke’s woes was the worsening trading environment in the UK caused by rising taxes and harsher regulations. In part, Lewis blamed the worsening UK backdrop for the Evoke failure.

Indeed, it was the announcement of the hiking of RGD to 40% in November that prompted Evoke to launch a strategic review.

Reeves insisted on Friday that it was the tax situation that had “brought about this opportunity.”

All your player base are belong to us: Reeves repeated the message from his company’s Q1 earnings that the company would be a net beneficiary from the changes in the UK, including April’s imposition of 40% iCasino tax, with its Jackpotjoy and Virgin Games brands taking market share from an exiting long tail.

“The UK regulation and the tax rate mean it is definitely going to lead to fewer operators in the market,” he said.

The disappeared: Previously, he said VIPs had left the UK market already and that the double-digit YoY increases in the UK business in April and May was proof that its brands were taking market share from an exiting long tail.

But Regulus was less convinced that the UK market has seen the full effect of the tax changes and how the generosity programs have changed with it.

“We are not convinced that VIP customers have entirely left the UK online gambling market; many are currently simply spread across multiple accounts, including the black market,” the team said.

But further regulatory pressure could eventually see them leave the market altogether. “A shrinking TAM could therefore be a bigger problem than market share gains,” they argued.

Fourth time lucky? Reeves noted that in buying Evoke, it is “saving us a bunch of time and is in line with our long-term plan.” Macquarie said the acquisition “makes strategic sense” given the geographic and product diversification and potential synergies.

But Regulus noted this is the fourth time someone has “attempted to fundamentally re-wire William Hill.”

A post synergy combination could find itself with very similar top-line and cost problems to Evoke as the next refinancing looms, they wrote.

“Buying time only works if top-line momentum is bought as well, and that challenge does not yet have a clear answer.”

M&A X-ray

The debt can: On Friday, E+M took a look at Bally’s Intralot’s deal for Evoke in detail. See the M&A X-ray edition (PRO subs only).

Octoplay and BetMGM have partnered to host exclusive Elvis Presley-themed content across North American markets. The collaboration connects Octoplay’s design with Entain’s global network, focusing on bringing iconic cultural themes to a broader audience through a shared infrastructure. 🌎

+More

The big mo: UAE-licensed Momentum has announced the launch of Play971, the emirate’s first and only sports-wagering and iCasino platform. Momentum said that Play971.ae would provide wagering opportunities across major international sports and leagues, alongside regional and local events, including UAE football and horseracing.

E+M PRO

Allwyn

Buy-ins: The consolidation of PrizePicks and the continuing contribution from the Betano business, where Allwyn has a near 37% stake, provided the highlights for a company that has newly established itself as a consolidated entity. The M&A schedule might have been even busier but for a regulatory ruling that put the mockers on the Novibet deal and has now prompted a €150m share buyback to utilize the otherwise unnecessary cash.

See the Earnings Extra edition sent this morning (PRO subs only).

Chart of the week

Betano’s growth: In Allwyn’s Q126 presentation, the company disclosed the revenue for the past two years of Betano. CFO Kenneth Morton said the business was “not only growing very quickly, but also highly cash flow generative.”

Goes up to 11: He noted how Betano was taking this momentum into the World Cup, repeating a comment from Betano’s CEO George Daskalakis that at the time of the last tournament the company had three markets represented at the event.

This year that will be 11.“That gives you an indication of the expansion geographically of that business over time,” Morton added.

Going by the figures, Betano achieved LTM revenues of €2.98bn.

Markets

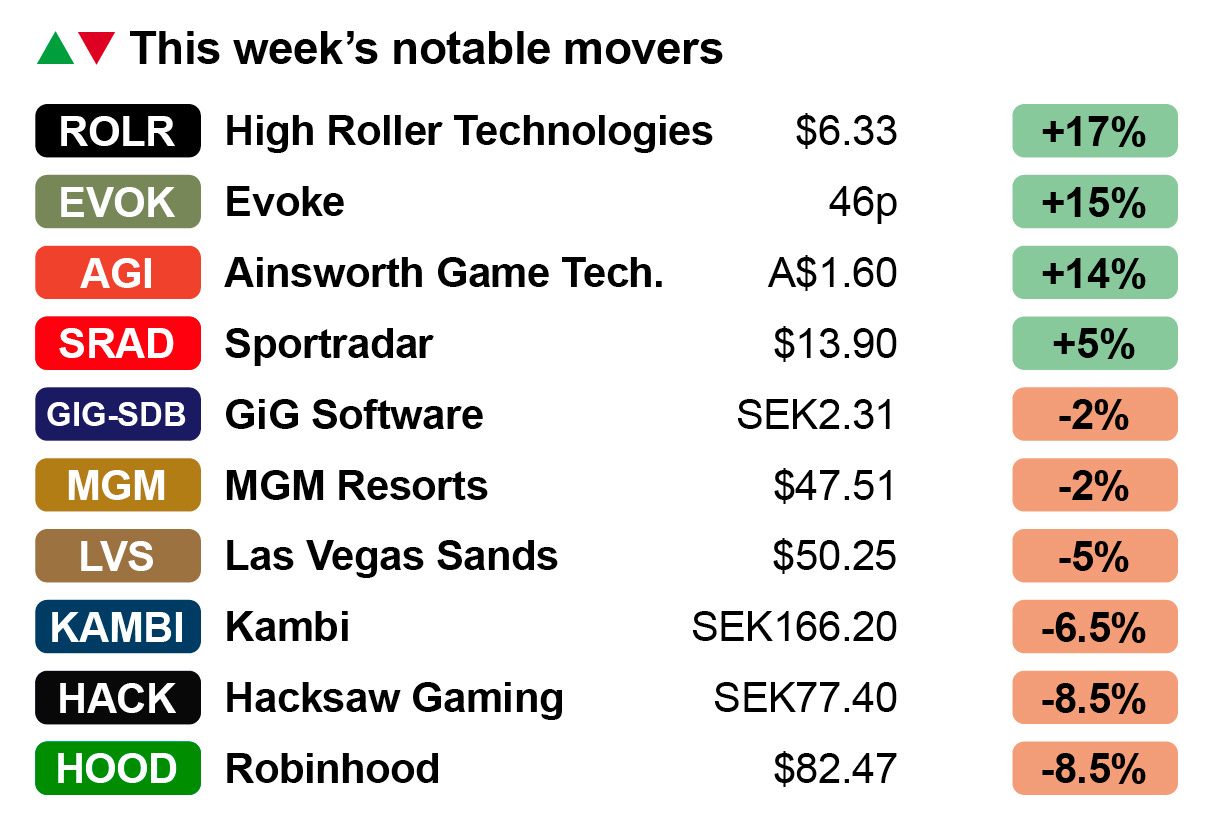

Unravelling: Ainsworth Game Technology soared 17% on Friday, leaving the company up over 14% for the week, after it announced the departures of chair Danny Gladstone and company secretary Mark Ludski.

The pair were the subject of allegations in the Australian Financial Review that they received millions of dollars in previously undisclosed bonuses shortly after Novomatic bought into the business.

The company said it was “in the best interests of AGT for them to resign” so that it can “move past these distracting complaints.”

Non-executive director Graeme Campbell has been appointed as the new chair while Lynn Mah, AGT’s CFO, has been appointed as interim company secretary.

She will be aided by the appointment of Andrew Kabega of BoardRoom, who, the company said, has a “depth of experience across ASX and ASIC compliance.”

Run, Forest, run: Separately, the company responded to a report that its US subsidiary was the subject of a suitability investigation by The Forest County Potawatomi Gaming Commission.

Ainsworth said that after careful evaluation of the responses and information provided by AGT US, the Commission found that it had “fully complied with all requests.”

It added that the company had been told that it had addressed “all concerns outlined in the review.”

The Commission renewed AGT US’ license on May 28 and confirmed that the license “remains in good standing.”

Favorite son: At the same time, Kjerulf Ainsworth, son of AGT founder Len Ainsworth, has increased his voting power in the Australian slot machine maker to 9.55% following a series of on-market share purchases and acceptances under his earlier proportional takeover offer.

A filing late last week showed Kjerulf Ainsworth buying a further 2m+ shares to up his stake from the just over 8% level revealed in March.

Does your Bet Builder supplier or in-house Same Game Multi solution support 12 sports, including all of the main global betting sports, plus local variants and even eSports? Does your product allow your end-users to place both Pre-Match and In:Play Bet Builders across multiple sports? Can you offer cashout across all Bet Builder transactions? Does your solution use your own odds rather than another opinion of the market? If the answer to any of these is ‘no’ then come and find out why over 200 operators are using the Algosport Bet Builder solution today.

World Cup puts+takes

Onside: Analysts appear to be converging on an awkward truth for the operators: the World Cup is a customer-acquisition event not a revenue windfall, and the latest preview from the team at Stifel was the most explicit yet on why investors should look through the handle bump.

Stifel forecasts a mid-single-digit percentage uplift to US OSB handle across Q2 and Q3, well ahead of the ~2-3% it attributed to Qatar 2022.

This is helped by the expanded 104-match format, a quiet North American summer calendar, better products and cleaner time zones for the host nation.

But it expects little of that to survive the accompanying promo and marketing spend on the way to EBITDA, and noted much of the 2022 lift was substitution from other sports, what DraftKings at the time called “a nice little boost.”

Offside: Working against the uplift: cannibalization of baseball and other summer handle, continued leakage to Kalshi and Polymarket, and shaky USMNT form, while Italy’s failure to qualify again dents a key Flutter market internationally.

Mind the gap: Others still see the World Cup generating big numbers and, just last week, Macquarie argued that global wagers would top $50bn and with a ~2-5% EBITDA uplift.

The team said that with the expanded schedule staking would run ~60% above the $35bn-plus it estimates was wagered in 2022, with further upside from parlays and player props.

Deutsche Bank previously put US handle at $4.1bn while Citizens argued for ~$25m of US EBITDA apiece for DraftKings and FanDuel.

All are arguing for plenty of top line but a thinner bottom line.

Sign here: Where the various notes agreed is user acquisition. Stifel cited SensorTower data showing roughly 2x app-download uplift in World Cup months and Spanish registrations up 57-74% in past tournaments.

The real prize, they argued, is a “ramp pull-forward” in high-growth states such as Missouri, North Carolina and Florida, and international markets such as Brazil and Mexico, plus re-activation of churned users in mature states.

Team sheets: On the stocks, Stifel kept Flutter as its preferred operator on depressed expectations and stabilizing FanDuel share, but called Codere Online the cleanest World Cup play given Mexico’s time-zone fit and rivals bet365 and Betano sidelined by a regulatory probe.

It rates affiliates and data providers the most attractive exposure on stronger flow-through, preferring Sportradar, with Gambling.com tagged the high-risk, high-reward option.

Their choice broadly echoed Macquarie’s tilt toward Flutter, Super Group, Rush Street and the same data names.

Further reading: See the World Cup Puts+Takes edition appearing later this week (PRO subs only).

Upcoming earnings

Jun 8: Evoke AGM

Jun 9: Codere Online Earnings Debrief

Jun 16: Penn Entertainment AGM

Jul 17: Evolution

Gambling.com Group [Nasdaq: GAMB] is fueling the online gambling industry with unmatched performance marketing solutions. Leveraging proprietary technology, a diverse portfolio of premium websites, and the newly acquired consumer-facing OddsJam and B2B service provider, OpticOdds, $GAMB connects operators to high-value players across the globe.

Positioned as a dynamic leader in the sector, Gambling.com Group is an engine of growth and profitability, backed by a proven track record of driving revenue for operators in sports betting, iGaming, and beyond.

Visit our investor page to see why it’s the platform behind the industry’s most successful operators.

An +More Media publication.

For sponsorship inquiries email scott@andmore.media.