Resolution of BetMGM ownership must come soon.

In +More: Spribe’s Aviator warning.

Markets watch: Investors desert Star Entertainment in January.

By the numbers: Last month was disappointing in Macau.

Hard Rock Bet is gearing up for 2025 with a focus on amplifying brand and product engagement. With a powerful, custom-built bonusing system and an ambition to redefine traditional CRM, we're seeking leaders who are driven to challenge the status quo:

And other amazing positions here

Stick or twist?

Can’t get used to losing you: Entain CEO Gavin Isaacs is now “more open-minded” about selling the company’s share of BetMGM to MGM Resorts, having been determined to maintain the JV when he first joined in the summer, according to industry sources familiar with Entain’s current thinking.

BetMGM will report its 2024 numbers tomorrow, Tuesday, after what was billed as a “year of investment.”

Jefferies is forecasting a narrowing of losses of $30m from $250m in 2023.

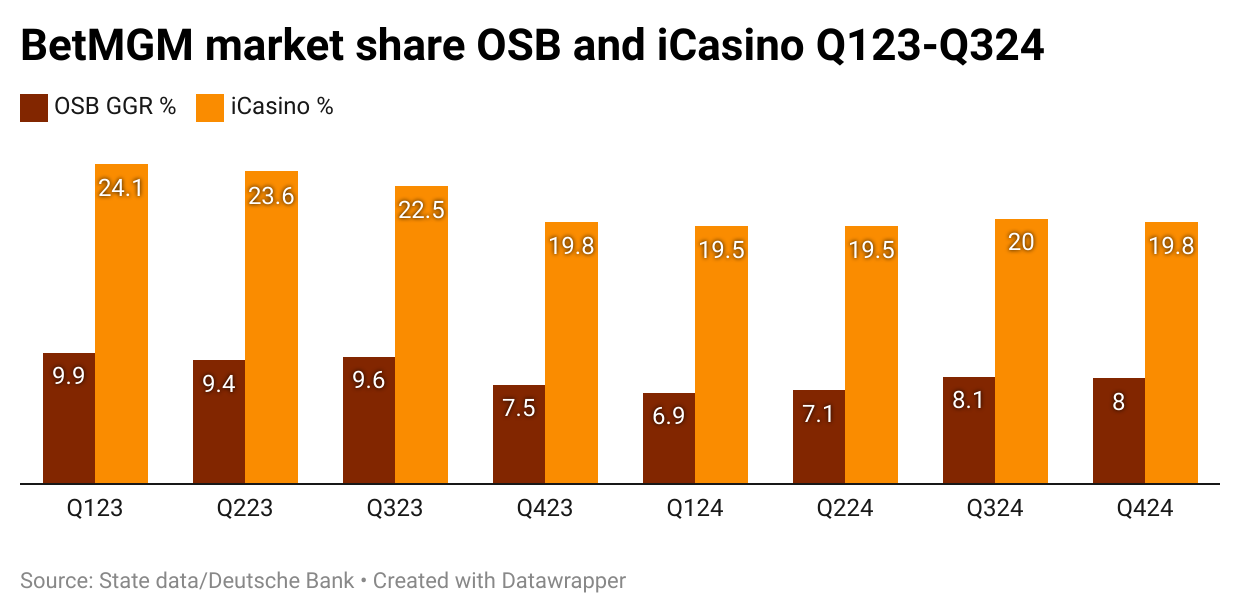

Let me leave or let me love you: Central to the debate is the performance of the business, which in terms of OSB and iCasino market share has been lackluster, even if it has managed to pull itself out of a marked decline in H124.

Finding the bottom: On the call with analysts for Entain’s Q3 trading, CFO Rob Wood noted BetMGM had achieved market share “stabilization” after it enjoyed 18% growth in Q3. This came after anaemic growth of 3% in Q1 and 9% in Q2.

The blended market share at the time grew from 13% to 15% by the end of Q3.

But Wood noted the uplift reflected a heavier dependence on iCasino during the quieter summer months for sports betting.

The secret of my success: Jefferies suggested BetMGM’s improvement has been helped by the integration of the pricing capability from Entain’s Angstrom unit into the BetMGM sports offering.

The team added that, as a result, BetMGM exited 2024 with OSB market share rising and “having delivered its highest growth in over two years.”

Eminent thinkers: Key to the thinking within Entain is the position of activist investor Eminence Capital, which holds a near 6% stake and has CEO Ricky Sandler on the board.

“Eminence is US-centric and may feel that they want Entain to have a US position,” said an advisor source. “But they are also likely to be very pragmatic.”

“Looking at it with a critical eye, it's not clear to me that BetMGM is a winning asset for Entain,” the source added.

Mom and Pop: Sources pointed out the structure of the JV, with BetMGM’s management reporting to two parents, has always been suboptimal.

“The current structure must be holding them back,” said the advisor source. “Decision-making is genuflecting to two different owners.”

“Compromises happen when you really can’t afford them in such a fiercely competitive market.”

I want it all: On the MGM side, the company has never made a secret of the fact it would prefer to own 100% of BetMGM. But following the aborted attempt to buy the whole of Entain in January 2021, it has been circumspect about how it was going to achieve this goal.

“MGM just has to make BetMGM work in the US,” said an industry insider.

“If they don’t get it right, the share price won’t be driven by any success it has with BetMGM elsewhere in the world. Everything else is a sideshow.”

Deep and wide and tall: The elephant in the room is the question of price. The industry insider admitted there remains a “chasm” over valuation, but with the “channels always open” between the two companies – partly facilitated by investment bank Moelis – the potential is there for a resolution to be found.

“How long can you drag this out for? At the end of the day, we all know MGM is going to end up owning this thing,” said the industry insider.

Leaner and meaner: Plus, Entain could use the money to reinvest in the rest of the business. “The thinking internally is that it is underweight in other markets,” said the advisor source.

“If it happens, it could lead to a really focused business and investors would be sharing out a $1bn+ return to shareholders and that would buy really good goodwill.”

“The board might find that very compelling.”

Or, as the industry insider put it: “Everything has its price. There are no sacred cows.”

Venture capital firm Yolo Investments manages in excess of €500m in capital across 100 exciting fintech, gaming and blockchain companies. The Yolo Investments' Gaming fund, regulated by the Guernsey Financial Services Commission, has taken positions in fast-growth suppliers and operators, including Dabble and Enteractive. Yolo Investments (yolo.io) wants to hear from readers of this newsletter. Get in touch with your pitch, or for a chat about innovative products which can plug into our investment ecosystem.

Earnings Extra

The week ahead: BetMGM’s FY investor update will be the subject of an Earnings Extra edition on Tuesday following the call with analysts.

Further Earnings Extras will be sent following Betsson’s Q4 earnings on Thursday morning and on Friday after Boyd Gaming’s call AMC on Thursday.

Any subscribers who wish to upgrade to the E+M PRO package to receive Earnings Extra editions can do so via the subscription page. A subscription costs £99 a month ($120) or £999 a year ($1,200). Discounted group subscriptions are also available.

+More

The company behind the popular crash game Aviator, Spribe, has issued a statement via LinkedIn warning that “unauthorized third parties” are approaching its clients trying to sell them a knock-off version of the game.

It added that any operator or partner “hosting or distributing these games will be in direct violation of our rights and may be subject to legal action.”

This comes after Aviator LLC, owned by ex-Adjarabet owner Teimuraz Ugulava, issued a press release saying it had settled a legal dispute with Flutter over the use of the name.

White Hat Gaming is considering a sale of its studios unit, according to a report from Next.io. The site suggested a buyer has “been identified.”

Earnings in brief: Australian horse-racing betting technology provider BetMakers saw Q2 revenue decline 6% to A$20m ($12m) but improved its adj. EBITDA losses to just A$0.3m, helped by lower costs following a recent restructuring.

On social… an analyst throws in the towel.

Market watch

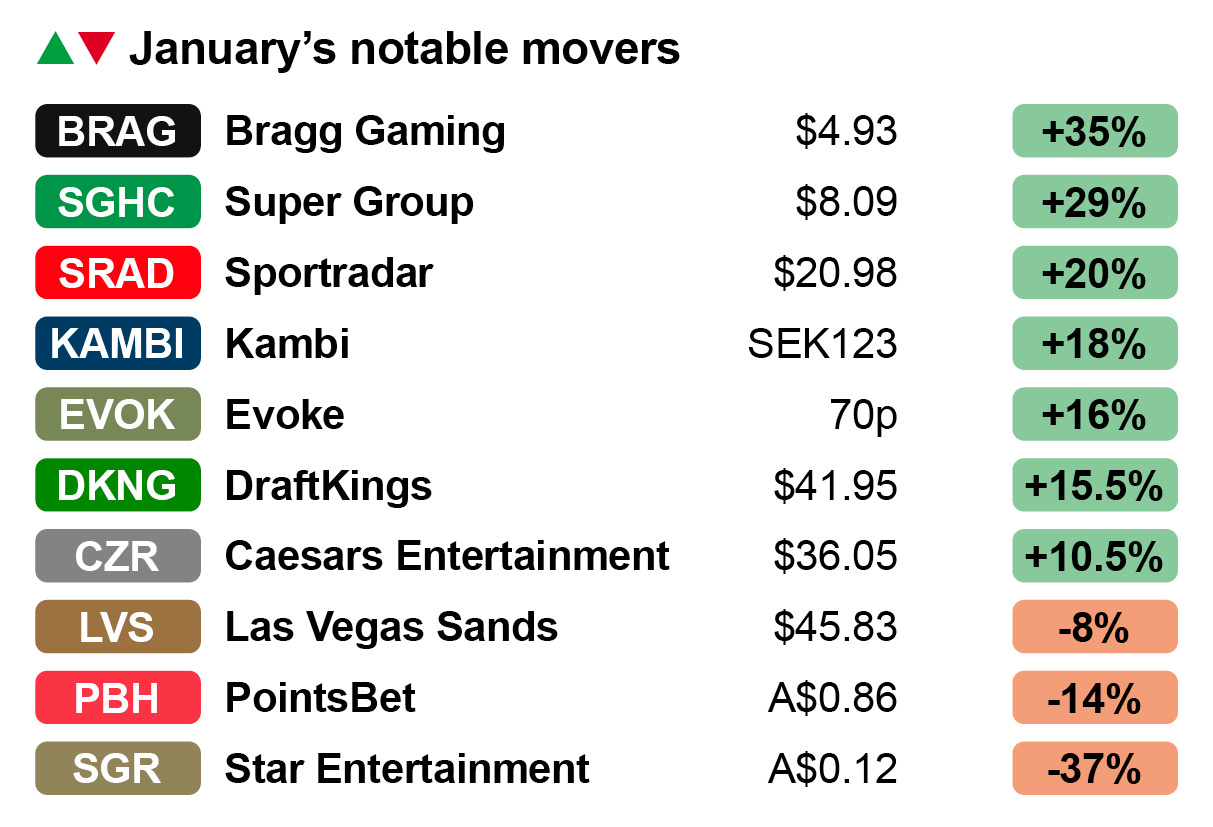

You make me sad with your eyes: Star Entertainment has been under pressure in the past month on fears that the company might be running out of cash. Suitably worried, shareholders have deserted the stock, which has fallen 37% since the start of the year.

The situation improved marginally within the past week with the share managing a 4% bump up.

This came after the company announced it had sold its Star Sydney event center and some additional space within the casino property to Foundation Theaters for A$60m ($37.4m).

Get my point: Staying in Australia, PointsBet was down 14% for the month after suffering a near 13% fall on Friday following poorly received earnings that showed turnover volatility in Q2, even as the hold and EBITDA picture improved.

Earnings Extra covered PointsBet’s earnings call on Friday.

Enjoying a far better month was Betway and Spin brand operator Super Group. After releasing preliminary Q4 numbers, the company saw its share price soar 29% for the month.

Recall, the company said towards the end of the month it expects to report record quarterly revenues of ~€486m and adj. EBITDA of €125m-€130m.

Bragging rights: Topping the tree this month was online gaming supplier Bragg Gaming, which got a boost from the announcement of a new content and tech partnership with Caesars Entertainment.

Paying the premium: DraftKings investors seemingly warmed to the company’s unveiling early in January of a new paid subscription option (there’s a lot of it about) to be offered initially in New York.

EKG noted that the New York authorities have already given the new offering a pass, saying that subscription revenue would not be taxed as gaming revenue.

Lap of luxury: It is a “major policy success,” the EKG team said, who added they “lean positive" on the product though they do see it as being a product that has low barriers to entry should it succeed.

EveryMatrix delivers iGaming software, solutions, content and services for casino, sports betting, payments, and affiliate/agent management to 300+ global Tier-1 operators and newer brands. The platform is modular, scalable, and compliant, allowing operators to choose the optimal solution depending on their needs.

EveryMatrix empowers clients to unleash bold ideas and deliver outstanding player experiences in regulated markets.

Analyst takes – Penn Entertainment

Reaching the Pinnacle: Taking a look at the alternative slate of board nominations put forward by activist investor HG Vora last week, the analysts at Jefferies said the candidates have the “relevant credentials.”

Notably, one of HG Vora’s nominees, William Clifford, was previously CFO at the then Penn National Gaming from 2001-13.

Carlos Ruisanchez, meanwhile, was CFO at Pinnacle Entertainment during its acquisition of Ameristar Casinos and the subsequent sale of its real estate to GLP and operations to Penn.

Change is gonna come: As to what happens next, the Jefferies team said that, regardless of the outcome of HG Vora’s boardroom challenge, a “change in strategic priorities” is likely.

They expect to see “more emphasis on the land-based business and a repositioning of ESPN Bet.”

More takes

Las Vegas Sands: The analysts at CBRE suggested LVS will outpace a Macau market, which itself will see further growth this year, as the company sees the benefit from more of its room inventory becoming available following the renovation work at the Londoner.

The team at Jefferies slightly downgraded their estimate for LVS in 2025, predicting revenue for the year at $12.2bn and adj. EBITDA of $5.04bn.

By the numbers – Macau

Mis-firing fireworks: GGR for January came in down 5.6% YoY at $2.27bn, as the hoped for boost of Chinese New Year occurring at the end of the month failed to ignite the market.

The CNY period began on January 28 with celebrations running until tomorrow, Tuesday. It is expected that Macau will see 5 million border crossings over the period.

The team at Jefferies are optimistic over visitor numbers, noting comments from the head of Macau’s tourist office that they expect occupancy to be at >90% during the holiday.

24 in 24: Growth for 2024 came in at, appropriately enough, 24% YoY and the analysts at Seaport suggested that following this “strong” performance growth will moderate in 2025 to ~7%.

The 2024 growth left the market at 63% of 2019 levels and the Seaport team forecast that metric to rise to ~95% by 2027, as the market grows to be worth $34.4bn in GGR.

Challengers… (Re-)Assemble! 💥

GeoComply and Citi are excited to bring the Challenger Series back to New York during NEXT.io’s NY Summit on Tuesday, March 11th!

Learn first-hand experiences from gaming founders on high-growth tips and network with the most influential investors, founders, and leaders.

Earnings calendar

Feb 4: BetMGM

Feb 6: Betsson, Boyd Gaming

Feb 11: Catena Media, Red Rock Resorts

Feb 12: MGM Resorts

Feb 13: DraftKings, Wynn Resorts

Most operators can't afford to invest endless resources into fraud prevention while remaining competitive.

Luckily, sophisticated fraud protection is accessible with the right payments partner through a single integration.

Extended fraud protection: Vast coverage of fraud signals with device intelligence, user behavior analytics and more

Community data: Compare payment data against a rich network of iGaming, airline and e-commerce transactions

Risk scoring: Leverage machine learning to evaluate the likelihood a transaction will result in fraud

Start fighting fraud a smarter way while reducing the cost of accepting payments with PayNearMe’s all-in-one payments platform built for the iGaming industry.

An +More Media publication.

For sponsorship inquiries email scott@andmore.media.