19 May: Catena talks up incubator markets +More

Catena Media Q1, NeoGames earnings call reaction, Pollard Banknote Q1, Pennsylvania and Louisiana April GGR

Welcome to today’s newsletter. This morning, the top story comes from super-affiliate Catena Media where the Q1 results show it benefiting from the new state openings in the US. Then we follow up with the NeoGames earnings call review from late last week and, staying with instant win lottery products we have the Q1 numbers from Pollard Banknote. We also have data from Pennsylvania (sports-betting and igaming) and Louisiana. But first, the “exceptional” figures from Catena.

Please note that tomorrow’s newsletter covering Acroud and Genius Sports will be sent in the afternoon UK time.

If you were forwarded this newsletter and wish to subscribe, please click here:

Catena Media

The top line

As prefigured in early April, Q1 revenues soared 53% to €40.7m while adjusted EBITDA nearly doubled to €25.1m. Operating cash flow increased by 85% to €20.8m.

Revenue derived from casino rose 54% to €25.3m (62% of total) while sports revenue was up 64% to €14.4m (35% of total). Financial trading revenue fell 27% to €1.1m (3% of total).

NDCs rose to 157,546, up 31.8% to a new all-time quarterly record. However, casino NDCs were down 1% YoY to just over 76k while sports NDCs rose 91% YoY to over 80k.

Revenue from the US rose 200% to €22.4m or 55% of Q1 total helped by state launches in Michigan and Virginia. Post-quarter end Catena announced the $39.6m acquisition of US-facing Lineups.com. Pro-forma it would have been worth circa €2.2m in Q1.

Post-quarter revenue growth was 15% up YoY, 24% ex-Germany. Management noted this was against a very strong comparable.

Giant steps: CEO Michael Daly spoke about three types of markets for Catena: growth markets (US, Japan, Italy), mature markets (Sweden, UK, Germany) and then the incubation phase markets which includes Latin America, Asia and the US and Canada. He spoke about the potential from the “giant states” including New York and Florida. “We already operate in all these states because it is a matter of when not if they regulate and we will be the leader there. We see great potential and that is just looking at the sports-betting landscape. Consider that many of these states will also add casino.”

One-hit wonders: Asked about the one-time hit that comes from the opening of new states (as evidenced by the rising CPA percentage of revenues), Daly admitted that “you do see an influx”.

“But it also means that post-that influx, there is also a higher run rate,” Daly added. “It is difficult to project what that run-rate looks like now we have entered the off season (for US sports). Until we reach the start of the football season, we expect a higher base run rate but it might be early to say how much higher that is.”

Daly reiterated the importance of seeing growth in existing states in order to organically fund expansion into new states.

Dog eat dog: Against the backdrop of large-scale M&A in the US market - Better Collective's $240m acquisition of the Action Network springs to mind - Daly said the multiples were “quite high.” As regards further M&A involvement, he added that “as you would expect for pretty much any strong product in North America, we wouldn’t be the only ones looking at it.”

“The best competitors are often the small competitors. We are seeing (existing) competitors also buying other competitors. We’re not seeing a lot of new entries.” However, Daly was mindful of the low barriers to entry in the affiliate world. “There isn’t a deep moat between different affiliates; it’s how you execute and we think we are the best at that.”

Old world problems: Daly said revenues derived from Germany were down by more than 50%, a trend which has clearly continued into the second quarter. A question that will remain unanswered for now is whether the market post-July 1 is any different in revenue terms for the affiliate sector. Daly only said that the outcome later in Q3 and Q4 was still “unclear”.

Debt reduction: Catena Media is on a “significant debt reduction journey,” said CFO Peter Messner. That includes a refinancing. As a result of strong cash generation, the debt leverage has been reduced. He said the company was now in a “much better position” and it is now exploring refinancing opportunities on the bond repayment that would otherwise be due in May 2022.

NeoGames Q1 analyst call

The top line

Recall, last week iLottery specialist NeoGames published strong Q1s: revenues up 46.5% to $13.3m, share of revenues from the NeoPollard Interactive JV (see below) rose 736.5% to $8.2m. Total Q1 revenues were up 113.9% to $21.5m. Adjusted EBITDA increased 147.9% to $9.7m, earnings per share was $0.16 compared to a loss of $0.04, comprehensive income was $4.0m. Network NGR, which includes North America and Europe, increased 184.8% to $195.8m.

Parallel lines: During the analyst call on Friday CEO Motti Malul said the launch of iGaming and online sports betting in Michigan hadn’t cannibalised online lottery revenues.

“Michigan shows that iLottery can thrive in parallel with OSB and iGaming. Data also reveals similar dynamics in Virginia, New Hampshire and in Europe,” Malul added. Major Powerball and Megamillions jackpots had increased traffic to the group’s lottery partners, which helped them cross-sell to instant games.

Nsync: Referring to the ongoing digital shift happening in the US and other markets, Malul said states that had seen the strongest growth in iGaming and OSB were also the biggest iLottery states for Neogames. Analysts at Truist Securities were upbeat about the group’s prospects as “the only pure-play iLottery provider and market leader – seeing catalysts around state iLottery legislation, contract wins” and upside to NeoGames’ relationship with William Hill-Caesars Entertainment. They raised their guidance to $73-77m from $65-69m.

Instant hit: Instant games performed strongly and states with the full range of games (instant and draw) had strong quarters, “but even where there are only draw games, revenues are up threefold because we work hard on maximising our clients’ revenues,” Malul said.

No guidance or M&A: The company didn’t provide guidance for 2021, Truist upped its forecast to $73-77m vs. $65-69m previously. NeoGames has $98m in cash, but Malul played down talk of M&A, as a newly-listed group it was too early to talk of acquisitions.

Pollard Banknote

The top line

First-quarter record sales hit C$112.2m up 10% YoY. Sales including the proceeds from the NeoPollard JV (see above) hit C$122.1m, up 18%. Adjusted EBITDA up 45% to $23.3m YoY.

Long-term partner the Ontario Lottery announced in early April it was taking up the renewal option for the supply of the majority of instants until at least 2032. Meanwhile, Loto Quebec and the Michigan Lottery also extended deals and Idaho Lottery announced Pollard as their primary supplier for the next two years with six years of possible extensions.

The company successfully raised C$34.5m from a rights issue during the period. The company said M&A would play an “important role” in the future. The company recently completed the buyout of the Next Generation Lotteries business and pull-tab business Compliant Gaming.

Open society: The core instant win business continued to benefit from higher sales despite the headwinds of the pandemic as US lottery sales generated record revenues. The trend has continued into the current quarter as more retail venues across the US open up. The Charitable and Diamond Games business units rebounded strongly after the Q1 closures. iLottery sales rose threefold, helped by “robust” growth from newer contracts in Alberta and Virginia.

Pennsylvania April GGR

Sports betting GGR dropped 12% to $36m ($26.3m net of promotions) as the sporting calendar slowed down. iCasino GGR of $92.7m meant a 115% rise YoY but a 5.1% MoM drop.

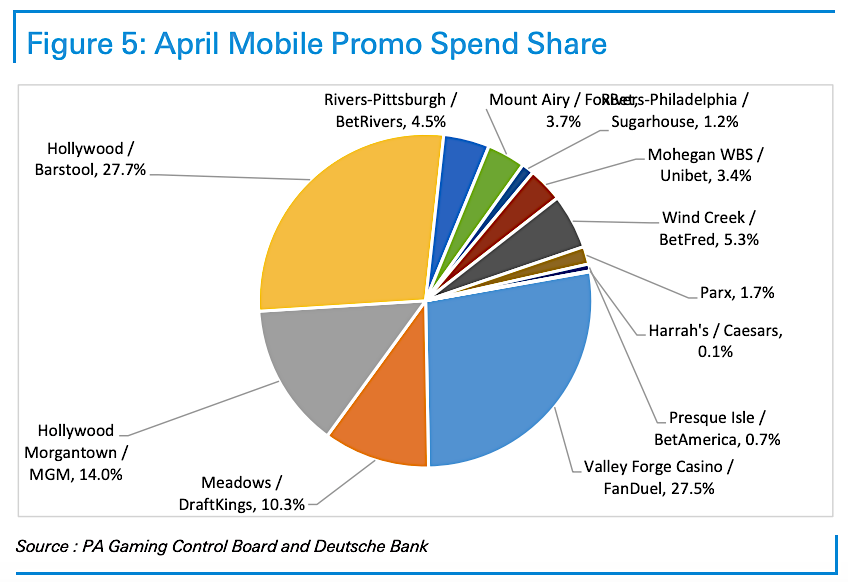

Sports betting: Handle fell 14.4% sequentially at $479.4m, mobile handle represented $439.1m of the overall figure, a 14.6% MoM drop. April hold was 7.5% vs. 7.3% hold in March, monthly mobile hold was 7.1%, retail hold was 11.9%. FanDuel and DraftKings continue to dominate mobile handle share at 62.2%.

Barstool was third with 13%, a MoM rise of 60 bps, but its share of promotional spend was 27.7% of the monthly total (see graph below). Barstool’s mobile promotional spend more was slightly higher than FanDuel’s, but the latter generated roughly “three times the mobile handle of Barstool,” according to analysis by Deutsche Bank.

BetMGM entered the PA market in December and recorded 7.5% share of mobile handle (vs. 7.3% in March and 7.2% in February). BetMGM promotions as percentage of mobile handle were up to 4.1% from 3.7% in March, “after two months of aggressive promotional activity in January and February.” FanDuel dominates YoY mobile market share at 41.9% and MoM at 44% with DraftKings in second at 19.4% YoY and 20.6% MoM.

iCasino: With online casino market share grouped by property license, tracking share by operator is difficult to do accurately. “For example, both DKNG and BetMGM roll up into Penn. In December, these two operators represented roughly 83% of the Penn skin revenue,” said Deutsche. Using similar percentage figures for each, the analysts estimated that Rivers led the market with a 28.8% share in April, followed by DraftKings at 21.3%, FanDuel at 16%, BetMGM at 8.9%, and Mount Airy (FoxBet) at 7.5%.

Louisiana April GGR

Louisiana’s casino GGRs rose 4.8% MoM to $235.8m in April. This represented a 18.2% rise on April 2019 numbers. Daily GGR was up 8.3% sequentially.

The GGR rise vs. April 2019 came from a 77% rise in daily spend vs. of +35.6%, “as we had assumed spend per visitor would average February and March levels versus 2019. Instead, it blew through February and March levels,” said Deutsche.

Penn National’s properties led the field and generated $87.9m of the GGR total, a 39.1% rise vs. 2019 and a 5.8% rise MoM. Boyd Gaming was second with $43.8m, a 10.3% vs. 2019 but down 0.9% sequentially. Caesars Entertainment came in a close third with $43.2m GGRs, a 10.5% drop vs. 2019 but up 7.8% MoM.

Newslines

Flutter-owned FanDuel said it would be hiring at least 900 people and investing up to $15m in a new product development office in Atlanta, Georgia, according to a report from AP.

On social

Twitter, show me the US operator preference for CPA over revenue-share:

Earnings calendar

20 May: Acroud, Genius Sports

24 may: New Jersey Q1

25 May: Gamenet/Lottomatica

Contact us

Scott Longley scott@clearconcisemedia.com

Jake Pollard jake@openmediaservices.com