Lit

Kalshi and Polymarket electrify the funding arena

Prediction markets duo’s valuation velocity rivaled only by AI giants.

In +More: BetMGM lowers guidance, High Roller confirms Crypto.com deal.

Startup funding rounds and buyout activity announced in Q1.

Money, pivots and predictions: the state of betting and gaming startups in Q1.

Hard Rock Bet is growing – we know you know! And we want to bring in some more maestros to make beautiful music in our Sportsbook. You need to be among the very best in the industry to be considered for these roles. Are you up to it?

Electrified

That’s how it starts: In terms of origin stories, Kalshi – ‘everything’ in Arabic – is quite the tale. Founded in 2018 by Tarek Mansour and Luana Lopes Lara, a pair of MIT grads, the prediction markets startup has defied both the federal government and state gaming regulators, and stormed the sports betting and financial citadels.

Having recently closed a $1bn funding round led by Coatue Management, it is now approaching an AI-type valuation of $22bn.

Its rival Polymarket, meanwhile, is reportedly targeting a similar outsized valuation, having just received a $2bn cash injection from Intercontinental Exchange (ICE).

Taken together, these two companies, which the world had barely heard of two years ago, can now claim valuations that are approaching a combined $44bn.

This is way in excess of the current market caps for OSB leaders Flutter Entertainment and DraftKings, of $18.4bn and $11.2bn respectively.

You check the charts: The volume numbers that underpin these valuations are genuinely striking. Bank of America’s profile of Kalshi noted that weekly trading volume has surged from roughly $100m a year ago to over $3bn today, making it one of the fastest-growing non-AI companies in America.

And start to figure it out: The bank calculated that at a $22bn valuation, Kalshi trades at approximately 15 times its annualized revenue run rate of $1.5bn.

This is a premium to listed exchange peers such as ICE, which trades at around 10x-11x revenue.

But it is not an outlier by the standards of high-growth private tech.

And if it’s crowded, all the better: Sports has driven most of that growth, accounting for roughly 80% of Kalshi’s volume. The platform peaked at number two in the overall App Store on Super Bowl Sunday and has quickly built a two-sided business.

It has D2C trading on its own app, alongside a B2B exchange used by Robinhood, Coinbase and others.

BofA said Kalshi enjoys structural advantages, including 50-state regulation, a minimum age limit of 18 and it doesn’t pay state gaming taxes.

But if you’re worried about the weather: Davis Catlin, managing partner at Discerning Capital, said Kalshi’s valuation is in part driven by evidence of continued execution – those trading volume numbers – but it is frothy.

“It’s 10% continued execution and 90% investors chasing the latest hype cycle,” he told E+M.

“Bubbles rise and fall,” he added. “We believe prediction markets are valuable, but we think the hype and valuation is currently well ahead of reality.”

Then you picked the wrong place to stay: Evan Meyer, managing partner at Astralis Capital, shares the skepticism. “I personally find it hard to justify,” he said of the 15x revenue multiple.

“However, when adjusting for revenue growth against some of the existing listed exchanges or OSB stocks, then Kalshi starts to look more intriguing.”

It comes apart: Countering that is the challenge of probability-weighting regulatory outcomes. Catlin suggested investors might be forced to look at a different valuation framework, one that accounts for the “decent chance” that sports events are regulated away in the next five years.

Like it does in bad films: “If you set that at 50/50, then you should be willing to pay a valuation that adjusts for that risk.

Using the 10x ICE multiple as a benchmark, that would mean investors should pay around 5x today given the regulatory risks.

Under such a formula, Kalshi would be worth closer to $7.5bn rather than $22bn.

And to tell the truth: Yet, the broader context for these valuations is one of profound disruption to the established gaming industry. Joel Simkins, CEO of XST Capital, said predictions are the latest in a long series of new products that have periodically convulsed the sector.

But he is “personally skeptical” of $20bn+ valuations being attractive entry points.

Similarly, Chris Grove, partner at EKG, said Kalshi being worth more than DraftKings or Flutter “doesn’t quite track and speaks to some kind of dislocation.”

“Whether that’s the former being overvalued or the latter being undervalued is the tricky question,” he added. “Common shareholders rarely do well in any down-round exit.”

Oh, this could be the last time: Then there’s the regulatory risk. The news changes every day, but as BofA noted last week, the current state of play shows legal action is now pending in 14 states, with federal circuit courts considering cases in New Jersey, Maryland and Nevada.

Oh, if the trip and the plan come apart in your hand: BofA said the “magnitude of the jurisdictional dispute and conflicting decisions in federal courts” increases the likelihood that the Supreme Court may have to ultimately intervene.

But “full clarity” could take until late 2027 or early 2028.

You can turn it on yourself, you ridiculous clown: Meanwhile, the political winds could also shift: Donald Trump Jr. is a strategic advisor to Kalshi and an investor and advisor to Polymarket. The current CFTC chair is openly supportive.

Neither condition is permanent.

You’ll forget what you meant: Kalshi and Polymarket have quickly built real businesses with real revenue and genuine product-market fit, and the institutional interest is legitimate: Goldman Sachs CEO David Solomon confirmed the bank is spending time with both companies.

But the $22bn figure represents a price paid for a minority stake. Liquidation preferences and investor protections mean common shareholders would be last in line in any adverse exit scenario.

Meyer noted that growth equity investors who traditionally avoided the gambling space are now chasing prediction markets precisely because they are classified as financials and exchange businesses rather than gaming.

That reframing, he argued, is “a significant part” of why large ticket-writers who would previously have passed are now competing to get in.

Where are you friends tonight: The secondary market is feeling the pressure too. Meyer observed that small blocks of shares have been trading at prior round valuations or slight discounts and, with the new Kalshi round announced and a Polymarket raise rumoured, those levels are due to reset.

As Catlin noted, secondary buyers are currently willing to pay near-round prices simply because of FOMO.

But the question is not what these shares are worth today in a hot market.

Instead, it is what they will be worth in three years if sports contracts face a Supreme Court ruling, a CFTC policy reversal, or simply the gravity of a summer with no marquee events.

“Value creation is almost always a function of both substance and story,” Grove observed.

“It’s a lot harder to draw a clear line between the two than most people like to believe.”

Increase Operator Margins with EDGE Boost Today!

EDGE Boost is the first dedicated bank account for bettors.

Increase Cash Access: On/Offline with $250k/day debit limits

No Integration or Costs: Compatible today with all operators via VISA debit rails

Incremental Non-Gaming Revenue: Up to 1% operator rebate on transactions

Lower Costs: Increase debit throughput to reduce costs against ACH/Wallets

Eliminate Chargebacks and Disputes

Eliminate Debit Declines

Built-in Responsible Gaming tools

To learn more, contact Matthew Cullen, chief strategy officer: Matthew@edgemarkets.io

+More

High times: The recent share price rise of High Roller Technologies – up 73% since Friday’s close – might be explained by the news yesterday that it has reached definitive agreement with Crypto.com over the launch of a prediction markets offering. Under the terms of the agreement with Crypto.com | Derivatives North America, High Roller will offer its event contracts across all 50 states.

Picking up the slack: Betway has moved to secure a new partnership with the Jockey Club to mark its return as a sponsor of British racing. The company will be the sponsor for 16 days of racing this year, including the sponsorship of the July meeting at Newmarket, taking the place of former sponsor bet365.

Earnings in brief

BetMGM has lowered its FY26 net revenue guidance to $2.9bn-$3.1bn, down from $3.1bn-$3.2bn, and now expects adj. EBITDA to come in at the lower end of its $300m-$350m range. Q1 results showed only modest progress, with total net revenue up 6% YoY to $696m and adj. EBITDA up 11% to $25m. iGaming outperformed with 9% revenue growth, while average monthly active users declined 9%.

E+M PRO will report on the earnings call later today.

Deal talk

Traffic Lab’s management has completed a majority buyout of the Danish iGaming affiliate and B2B tech provider, shifting away from prior ownership under Capitalab. CEO Peter Gunni said the deal enables broader employee ownership. The transaction follows leadership changes after founder Sebastian Agerskov stepped down in 2024.

Does your Bet Builder supplier or in-house Same Game Multi solution support 12 sports, including all of the main global betting sports, plus local variants and even eSports? Does your product allow your end-users to place both Pre-Match and In:Play Bet Builders across multiple sports? Can you offer cashout across all Bet Builder transactions? Does your solution use your own odds rather than another opinion of the market? If the answer to any of these is ‘no’ then come and find out why over 200 operators are using the Algosport Bet Builder solution today.

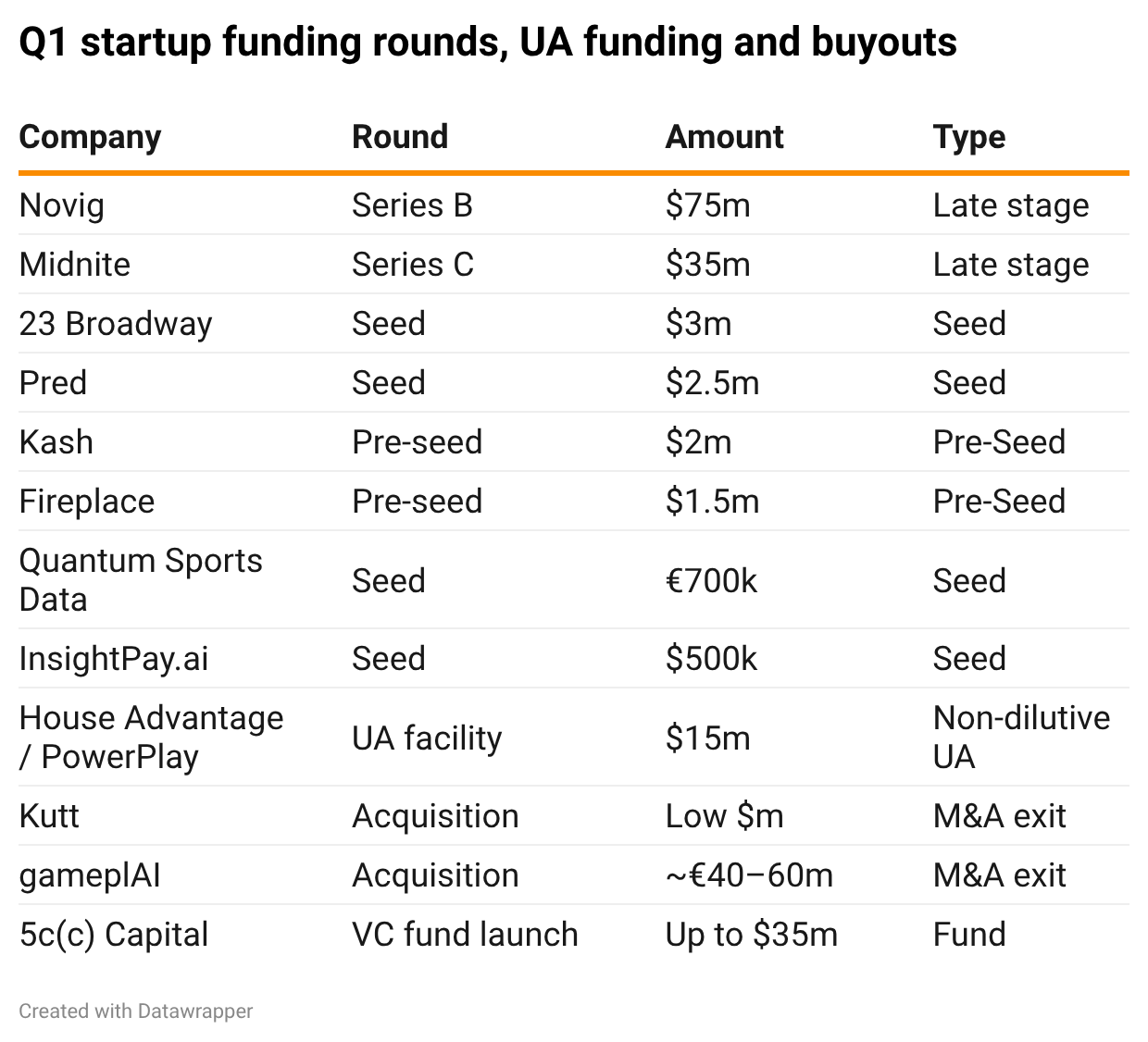

Venture playground – Q1 funding review

Crystal clear: Prediction markets is a subsector that is crystallizing fast, and the gravitational pull of Kalshi and Polymarket is now reshaping companies well beyond their own orbit. The most vivid illustration of this is Novig, which this quarter raised $75m in a Series B led by Pantera Capital at a post-money valuation of $500m.

This is Novig’s third business model in three years: having begun as a P2P betting exchange, it pivoted to sweepstakes in September 2024.

It has now pivoted again to seek a DCM license from the CFTC, as it repositions itself as a sports prediction market.

It is a story of founders reading the regulatory and capital environment with ruthless clarity.

The pivot attracted an entirely new category of investor: alongside Pantera, the cap table now includes Multicoin Capital, Makers Fund and Edge Equity.

Exchange the subject: These are names drawn from the crypto venture world that had not previously been associated with this part of the industry. The institutionalization of the sector took another significant step with the launch of 5c(c) Capital, named for the section of the Commodity Exchange Act governing prediction markets.

The fund, targeting up to $35m across around 20 portfolio companies, was founded by two Kalshi alumni.

It counts Kalshi CEO Tarek Mansour, Polymarket CEO Shayne Coplan, and Marc Andreessen among its LPs.

Separately, Fireplace, a professional trading terminal for prediction markets, raised $1.5m in pre-seed funding with the explicit aim of building “the Bloomberg terminal” for the space.

All about that Base: The Novig cap table is not an anomaly. Coinbase Ventures has now appeared in multiple funding rounds across the quarter, including the $2.5m raise by Pred, which is building a sports prediction exchange on Coinbase’s Base blockchain, and the $2m pre-seed for Kash, a social-native prediction market.

This follows Coinbase’s December acquisition of The Clearing House, a prediction market infrastructure business it had previously backed alongside Y Combinator.

Kutting crew: Kutt, the P2P social-betting platform that raised $1.5m in seed funding from Lightning Capital, was acquired this quarter by Bitcoin Depot, a Nasdaq-listed operator of Bitcoin ATMs making its first move into social betting.

The deal was in the single-digit millions, a modest exit, but the acquirer’s identity says something about where appetite is coming from.

The boundary between crypto infrastructure and betting infrastructure is dissolving, and capital is following.

Robot rock: Predictions aside, there is another theme running through the growth company coverage of the past quarter and that is artificial intelligence. But the applications are diverse enough that AI as a label obscures more than it reveals.

AxiumAI is delivering AI-driven real-time player engagement for sportsbooks.

The Fortune Engine is using AI math-solving tools to make the creation of burst-style games commercially accessible for studios of any size.

Approvely has built an AI-driven chargeback and fraud prevention system into its payments infrastructure.

Handigraphs launched an AI agent at the center of its product suite ahead of the MLB season.

23 Broadway, which closed a $3m seed round, has built its Atlas AI system to calculate optimal customer acquisition cost and predicted long-term value for gaming operators.

plAI maker: The quarter also featured a headline-grabbing acquisition as Kaizen Gaming, the operator behind Betano, snapped up AI-assisted sports-trading provider gameplAI for a figure sources put at between €40m and €60m.

The deal fits a well-documented pattern of operator consolidation in sports trading.

It follows PointsBet’s acquisition of Banach Technologies, Entain’s purchase of Angstrom, and DraftKings’ acquisitions of SportsIQ and Simplebet.

Pure gold: One of the more structurally significant developments of the past year has been the emergence of non-dilutive user acquisition financing as a distinct product category.

House Advantage, the JV between Discerning Capital and PvX Capital, has in six months announced loans supporting up to $150m in advertising spend.

It has signaled it expects to more than double that figure in 2026.

Its latest partnership, a $15m facility for Canadian operator PowerPlay, illustrates the model: 24 months of player acquisition and brand building funded by debt rather than equity.

That model is attracting competition. 23 Broadway raised its $3m seed explicitly to build a rival integrated platform, combining non-dilutive capital with its Atlas AI system.

Do it yourself: Some of the most interesting companies covered across the quarter by E+M’s in focus feature are yet to raise externally, and that itself is a data point.

Avanti Studios, the next-gen live casino supplier co-founded by LeoVegas founder Gustaf Hagman and Authentic Gaming founder Jonas Delin, has been funded by the founding team and one strategic investor.

Approvely has been funded entirely by operating cash flow and reached profitability without institutional support.

Bettortainment, the live-betting watchalong content provider launching out of Leeds, is bootstrapped but actively in conversations with investors.

The Fortune Engine, the Brisbane-based SaaS platform enabling burst-style game creation, is planning to open a seed round by mid-2026.

These are companies at the pre-institutional stage, but given the trajectory of the sector, it is unlikely to be a long wait.

We asked traders what they actually needed. Then we built it. OpticOdds Screen V2 gives you customizable layouts with MyView, real-time and historical odds side by side, and smart alerts that cut through the noise so you can act faster.

Get access NOW.

Upcoming earnings

Apr 15: Rank

Apr 20: Bally’s Intralot, Plus 500

Apr 22: Evolution, Churchill Downs (earnings)

Apr 23: Penn Entertainment, Churchill Downs (call), Boyd Gaming

Apr 24: Betsson, Gaming & Leisure Properties

Octoplay is live in Spain! 🇪🇸 By bringing its premium slot portfolio to the region, the studio further solidifies its position as a key player in the European iGaming landscape.

An +More Media publication.

For sponsorship inquiries email scott@andmore.media.