Room at the top: price holds key to Tier 2 competitors

HoldCrunch price data analysis, Games Global IPO prospectus, Vegas visitation +More

Data suggests a profitable middle tier in the US is possible.

In +More takes: FanDuel, Las Vegas Sands and 888.

An insight into the iCasino estimates in Games Global’s IPO prospectus.

The number of Southern Californian visitors to Las Vegas hits multi-year high.

Price point matters for Tier 2s

The price of success: The narrative around the top two in the US OSB market sharing an unassailable lead over the rest of the market is challenged by new data that suggests Tier 2 operators might yet find a way to succeed with market shares of between 10% and 15%.

Analysis by pricing data provider HoldCrunch shows price holds the key for second-tier operators.

The data points to evidence of success being enjoyed in this respect by BetMGM, showing it has benefitted from improving the prices offered to its sportsbook customers.

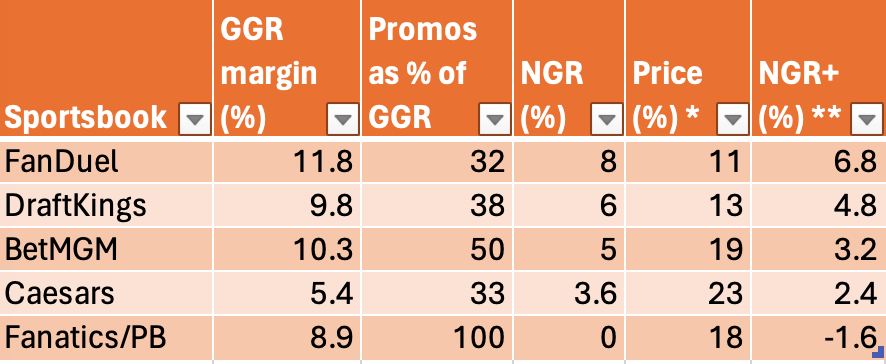

How did we get here? Looking at the data from the states that report at an NGR level, the HoldCrunch analysis shows which sportsbooks are offering the best prices to customers while at the same time returning the highest margins. The table below shows how in 2023 FanDuel and DraftKings led the major challengers by some distance on both of these price and margin metrics.

States reporting NGR at an operator level, Feb23-Jan24

Source: HoldCrunch. The NGR states in this analysis are AZ, CT, KS, KY (October only), MD, MI, OH, PA. Each operator's margins are calculated using only data from states where that operator is present

*The lower the percentage, the better the prices offered to customers. Data is from NBA, NCAAB, MLB, NFL, NCAAF

**NGR+ is NGR after taking account of the cost of equaling the leader on price (GGR minus 'the promo % plus the price %')

Some explaining to do: The first three columns of data are numbers everyone is familiar with: GGR, promos as a percentage of GGR and NGR. The fourth column, price, comes from the HoldCrunch platform and it shows who was offering customers the best prices (odds/lines). The lower the price % number, the better the prices offered to customers.

“You can see that FanDuel and DraftKings have been taking price seriously and offering customers leading prices; their price percentage is lower than the challengers,” says Tom Johnson, HoldCrunch founder and former VP at FanDuel.

“To be 0% you’d have to be best price in all markets pre-game and in-game,” he adds. “No one does that, so you’re looking for the lowest percentage and the percentage gaps between books to understand price.”

Why the market leaders lead: A 10% difference MoM is likely to move handle share. “FanDuel and DraftKings didn’t just lead on price; they made a point of staying very close to each other,” Johnson says.

“The last column is margin after taking account of not just promos, but the cost of equaling whoever the price leader was at the time,” Johnson explains.

“It is what we call NGR-plus.” The calculation is GGR minus the promo percentage, plus the price percentage.

“The bigger your price percentage, the bigger the hit to margin if you were to equal the leader on price,” says Johnson.

EveryMatrix delivers iGaming software, solutions, content and services for casino, sports betting, payments, and affiliate/agent management to 300+ global Tier-1 operators and newer brands. The platform is modular, scalable, and compliant, allowing operators to choose the optimal solution depending on their needs.

EveryMatrix empowers clients to unleash bold ideas and deliver outstanding player experiences in regulated markets.

Explaining the plusses

Snapshot: Johnson explains that two books reporting 10% GGR and 6% NGR might look the same, but if one is offering -111 on average and the other -109 their true margin performance is not the same at all. “NGR is a snapshot in time of profitability,” he says.

“NGR+ says ‘what’s this book’s true underlying margin performance when handle is stable through competitive prices?’”

“It is a more accurate measure of margin performance,” Johnson says, and FanDuel and DraftKings again came out on top as can be seen in the table.

“The market leaders didn’t just offer better prices, they retained higher margins after adjusting for differences on price.”

A change is gonna come: The table below is a more recent quarter, November 2023 to January 2024, and there are some significant differences:

States reporting NGR at an operator level, Nov23-Jan24

Holding the line: Johnson points out that the most notable price+margin profile change is BetMGM where the price % as calculated by HoldCrunch is almost 9%, which is in line with the best, in this instance FanDuel, which is on 8%.

At the same time, its NGR+ – that is the margin after taking account of both promos and the cost of equaling the leader on price – is substantially higher at 4.5% vs 3% over the course of the 12 months.

It is also close to DraftKings’ 5%, which, as Johnson says, is “especially impressive given their parlay mix is less.”

Recall, both JV parents at BetMGM have spoken about the improvements that will be brought to bear on BetMGM’s offering by Entain’s acquisition last year of Angstrom. Just last week, Entain’s interim CEO Stella David said during the company’s Q1 trading update call with analysts that the “tangible benefits” of Angstrom were “just starting to reach players now.”

CFO Rob Wood said “Angstromized” products were leading to an increased parlay mix and with that increased margins.

Meanwhile, in MGM Resorts Q4 call, CEO Bill Hornbuckle said adding Angstrom would allow BetMGM to “stick out more product” with more confidence and with greater speed to market.

Taking a view: Johnson says that it is important to look at both the price percentage and NGR+ together. “You want to see an ability to deliver competitive prices for customers but also high margins at the same time,” he suggests.

“It is the core of what a high-performing sportsbook does – offer great prices while returning profits.”

“I’m not saying BetMGM will take share from FanDuel and DraftKings,” he adds. “Rather, these twin metrics of ‘low HoldCrunch/high NGR+’ are a must-have baseline from which to compete and grow.”

He adds that only now is the market seeing a challenger with those characteristics and that is why he believes the possibility of a profitable middle group shouldn’t be discounted.

“Perhaps 2024 can be a new Year 1 for some, and one or more of the challengers will turn a corner,” he adds.

Further reading: Investors believe the race in US OSB is down to two competitors, says the team at Morgan Stanley.

Maximize your trading success in 2024 with OpticOdds’ real-time Odds Screen.

Built for operators with an emphasis on speed and coverage, OpticOdds offers:

Pre-match & in-play main lines, alternative markets, player props for the Big 6, soccer, and more

Create bespoke custom weighted lines on the screen and receive live alerts for line movement via Slack or Teams

Push format API offering real-time betting odds from 150+ sportsbooks: player props, alternate markets, injury data, historical odds, settlements, scores & more

Get in touch at opticodds.com/contact.

+More takes

Hindsight is a wonderful thing: The team at JMP reported that FanDuel CFO David Jennings felt it would have spent even more money on player acquisition in 2021 and 2022 now that it knows the level of rewards it is reaping from those customer cohorts.

Las Vegas Sands: Reacting to the company’s Q1 earnings last week, the team at Seaport Research Partners, said Sands continues to face an element of market share loss partly due to disruption caused by redevelopment work at The Londoner and the closure of the Macau Arena.

“While the next few quarters will see some disruption, we anticipate Sands to begin winning back some market share during the course of the year and into next year,” the team added.

They noted that base mass has “lagged recovery in Macau” relative to premium. “Once the base mass recovery accelerates, potentially into the summer months, Sands will be the lead beneficiary of this customer base,” the team argued.

Delivery hero: Following 888’s brief Q1 trading update, the team at Jefferies said that “delivery is now the focus.” After a tough comparison period in Q124 and guidance implying double-digit growth through the rest of FY24E, “execution” is now the big question. The team noted, though, that leverage remains high in the short term at 5.6x FY23 numbers.

Games Global’s iCasino hopes

A stretch: A somewhat unlikely forecast for the number of legalized iCasino states rising to 15 by 2028 and for revenues to top $20bn compared to the $5bn achieved in 2022 lies at the heart of the Games Global IPO prospectus released last week. As noted last week, the IPO is likely to be the largest in the sector this year.

Super six: Recall, the stuttering progress of iCasino legalization to date has seen only six states go down the regulated path – New Jersey, Pennsylvania, Michigan, Connecticut, Delaware and, most recently, Rhode Island.

The hoped-for augmented number of states, which are based on estimates from gaming data provider H2, would include New York.

The prospectus cites H2 as suggesting regulation in the state is “expected” in 2025, alongside Illinois and Indiana.

New York once again failed to include any iCasino measures in its latest legislative session.

Are you sure we’re on the right track? Commenting on X, Chris Krafcik from EKG said the estimate for 2028 “feels really, really tough – impossible even. I just don't see a path.” Still, Games Global insists in its prospectus that “there is potential for longer-term growth” if additional states legalize iCasino alongside SB.

“We believe the economic benefits experienced by US jurisdictions that have legalized other forms of gaming may create an incentive for future iGaming expansion,” it added.

Hit the north: Games Global’s confidence in its opportunities in the US is in part driven by the success it has enjoyed in recent years in Canada. It said revenues from Canada grew by 32% YoY in the nine months to Dec23.

Games Global has completed a number of acquisitions in recent years including the Feb24 deal to buy the B2B arm of Digital Gaming Corp from Super Group.

The company said that, following this deal, it now distributed 160 games in the US while it hoped to also launch a live dealer operation by the end of this year.

Golden roads

Can’t you hear the whistle blowing? The news that construction of the $12bn high-speed rail line between Las Vegas and Southern California has finally begun comes as the number of visitors to the city from the region is at a multi-year high.

According to the visitor data analyzed by the team at Morgan Stanley, the percentage of visitors from Southern California rose to 32% in 2023 from 27% the year previous.

The next biggest slice of visitors comes from other Western states at 27%, with 18% coming from the South.

🚆 ✈️ & 🚘 Where do the visitors to Las Vegas come from?

On the up: The team at MS pointed out that the recent strength in the GGR numbers in Nevada has been driven by the increase in spend per head rather than any absolute increase in visitation, which is actually down 5% on 2019 levels.

“The increase in spend has coincided with an uptick in both higher income ($100K+) and Southern California visitation relative to history,” the team noted.

Calendar

Apr 24: Evolution, Kambi, Kindred, Churchill Downs

Apr 25: Boyd Gaming

Apr 26: Betsson, Gaming & Leisure Partners

Apr 30: Caesars Entertainment

May 1: MGM Resorts, Bally’s

Kambi Group is the leading provider of premium sports betting technology and services, empowering operators with all the tools required to deliver world-class sports betting and entertainment experiences. The Group’s services not only include its award-winning turnkey sportsbook but also an increasingly open platform and a range of standalone sports betting services from frontend specialists Shape Games, esports data and odds provider Abios, and AI-powered trading division Tzeract. Together, we are limitless.

For more info, go to www.kambi.com

An +More Media publication.

For sponsorship inquiries email scott@andmore.media.