Something changed: MGM and Entain in the spotlight

Assessing the chances of a deal between MGM and Entain, Q3 transactions review, SKS365 runners and riders +More

Good morning. In this month’s edition of Deal Talk:

Bill Hornbuckle and Jette Nygaard-Anderson, respective CEOs at MGM Resorts and Entain, are likely to be all smiles when they take to the stage at G2E later today. But underneath the likely bonhomie lie tensions over the fate of the joint venture partnership with BetMGM and the potential of an M&A deal, which would be sector-defining.

Plus, a roundup of the transactions in Q3, headed by Light & Wonder’s successful deal to buy the remaining slug of SciPlay.

Lastly, we examine the likely outcome of the apparent multi-bidder battle taking place for Italian-facing SKS365.

Where would I be now, where would I be now if we'd never met?

When two worlds collide

The next high-level meeting between MGM Resorts and Entain takes place under the lights of the Venetian ballroom.

The end of the affair: When Contessa Brewer steps onto the main stage at G2E in Las Vegas today with her guests Bill Hornbuckle, CEO at MGM Resorts, and his counterpart at Entain, Jette Nygaard-Anderson, it’s a toss-up as to whether she will be playing the part of gentle interrogator or marriage counselor.

In his public statements, Hornbuckle has made it plain that his company would – in an ideal world – own 100% of BetMGM.

Analysts are convinced a potential bid for Entain very much remains on the table despite Hornbuckle’s public disavowal of such an approach.

Meanwhile, sources close to Entain suggested it is as much in the dark as the rest of the market about how and when an approach might come.

Moves afoot: Whispers were circulating just a few weeks ago that MGM was plotting a renewed approach, but external events would appear to have conspired to put any corporate action on the back burner for the rest of this year.

First, the September cyberattack has thrown a spanner in the works.

The financial damage is somewhat contained; MGM said late last week the attack will cost the company $100m in Q3 adj. EBITDA, losses that analysts say will be covered by insurance.

But the management time spent on dealing with the crisis will have seen other matters kicked down the road, likely until next year.

Yield of its own: Meanwhile, the financial backdrop has deteriorated in just the last couple of weeks. “The 10-year yield of Treasuries has spiked, bringing more bad news if anyone is hoping to raise cash right now,” says Chris Lynch, head of gaming and leisure on the investment banking side at Citizens Bank.

That has knock-on effects for any potential deal.

“The 10-year treasury currently stands at ~4.8%, its highest level seen since a brief appearance in 2007. Prior to that, you’d have to go back to 2001 to see levels this high,” Lynch says.

“While the absolute yield is notable given how long we’ve been in a low-rate environment, the speed at which we got here is really what is impacting markets.”

Lynch adds that the “reason this matters” is that Treasury yields are typically viewed as the risk-free rate of return.

“Thus, any investment with ‘risk’ must be priced at a premium to the ‘risk free’ rate,” he says.

“This has caused the cost of capital for virtually every market and every company to increase – this includes debt (bonds, loans), public equities and private equity/venture capital.”

** SPONSOR’S MESSAGE ** Calling all traders and syndicates at G2E Las Vegas next week!

Are you looking to no longer turn away large staking customers or are you suffering from one sided markets?

Introducing Matchbook Brokerage - the one stop shop for all your high stake requests at competitive prices! See some of our recent NFL quotes below:

NFL 2023/24 Week 3:

BAL -7.5 vs IND

$50k / 100k / 200k / 400k

-106 / -106 / -107 / -108

DAL vs ARI Over 43

$30k/60k/120k

-108 / -109 / -110

NYJ + 2.5 vs NEP -2.5

$70k / $140k / $250k

+101/+100/-101

-118 / -119 / -120

Email Jesse & Ronan to set a meeting at G2E Las Vegas next week:

jesse@matchbook.com & ronan@matchbook.com

Matchbook B2B, because the best price is for everyone.

Find out more at: www.matchbook.com/b2b

Entain’s dilemmas

Father of the bribe: Falling into the category of known unknowns is the overhang caused by Entain’s acceptance of a deferred prosecution agreement with the UK’s Crown Prosecution Service with regard to bribery allegations and its previous involvement in Turkey.

What is known is the quantum: Entain has set aside a provision of £585m against any DPA settlement.

What the market doesn’t yet know is what it is paying the fine for.

But as one source put it: “We know enough of the detail to know that it has the potential to be explosive”.

‘The Kenny poison pill’: The only further information came from rival 888. During the summer the company became unwillingly embroiled in an ultimately fruitless bid from a group of activist investors, including ex-Entain chiefs Shay Segev and, crucially, Kenny Alexander, which would have seen the latter installed as 888 CEO.

The bid fell apart following the intervention of the UK Gambling Commission, which put 888’s license under review purely based on the potential of seeing Alexander installed as CEO.

Clearly, the Commission has seen enough of the case against Entain and its former head to mean that even the sniff of a chance of becoming a high-profile CEO at another firm was enough to endanger its license.

“This isn’t a legacy problem,” said one source. “This is a problem in the here and now if regulators or prosecutors believe that to be the case.”

A touch queasy

Outrageous: The deal that might be said to have broken the camel’s back as far as Entain’s investors are concerned was the £750 acquisition of STS in June. What initially looked like just another bolt-on soon came under attack publicly from Entain shareholder Eminence Capital, which characterized the deal as “perplexing”.

It seemingly broke the spell as it has since become evident that Entain’s entire M&A strategy has been put on hold.

Last month’s Deal Talk wrote about how the company had provided a chart with its H1 earnings, attempting to explain its M&A strategy.

Sources suggested this pitch at openness might have been poorly received by investors.

“That chart didn’t make sense,” said one industry insider. “I’m sure they got a lot of investors saying ‘what was that?’”

No longer at the table: The analysts at Peel Hunt noted that Flutter’s recent acquisition of a 51% controlling stake in MaxBet in Serbia would have been natural territory for Entain’s Eastern European-focused JV with Emma Capital.

“Perhaps Entain has M&A indigestion or perhaps it has been encouraged to back off from M&A by investors,” the team wrote.

“The record on M&A isn’t looking so good now,” said one industry source.

“The share price reaction is telling; it has been on the floor for the last few months.”

The situation wasn’t helped by the Q3 ‘revenue’ warning at the end of September. “Let’s be clear,” said one analyst. “That was a profit warning.”

Said another industry source: “There is shareholder angst.”

“Saying ‘give us to November to tell you the story’ is about trying to justify their actions,” they added about the planned Q3 statement.

🤮 Entain share price action YTD is not a pretty picture

** SPONSOR’S MESSAGE ** The American Gambling Awards, the first awards program dedicated exclusively to the online gambling market in the United States, is produced by Gambling.com Group (Nasdaq: GAMB), a leading performance marketing company for the regulated global online gambling industry.

The Group champions the development of a responsibly regulated, competitive online gambling market in the U.S. and the Awards help bring positive attention to the leaders making this a reality.

A full list of the 2023 American Gambling Awards winners is now available at: www.gambling.com/us/awards.

MGM’s choices

Marriage story: Rumors surrounding the relationship between MGM and Entain have been circulating for many months. Indeed, something of an acknowledgement of the tensions came in August when during MGM’s Q3 earnings call Hornbuckle said “candidly” that with BetMGM “our product is not where we want it to be”.

Privately, those that have spoken to both companies think the frostiness is now at arctic levels.

“I think bridges have been burned,” said one sector dealmaker, pointing to the news of BetMGM being launched in the UK.

BetMGM has in recent weeks begun an extensive marketing campaign for the brand – yet Entain is notably absent from the cast list on that one.

Instead, the operation is being run as part of the LeoVegas business, using a Kambi backend for the sports-betting side.

“I don’t sense there is the willingness to really make a go of [the JV] anymore, not in its current form,” added the dealmaker.

Gonna get along with you now: MGM does have choices. Publicly, analysts have been speculating about the potential for MGM to renew its bid to buy Entain outright. “We still argue that an MGM/Entain tie-up makes sense, it is just a question of valuation,” said the team at Jefferies, even after the UK BetMGM news.

Analysts at Citi, meanwhile, said a potential bid was “plausible” given that more than six months have elapsed since Hornbuckle told analysts in February it was “no for now”.

Sources agreed that if an approach is to be made, an outright bid would be preferable to an attempt to buy out Entain’s half of the JV.

“When you look at the math,” said one dealmaker, “the fact that the Entain share price is depressed makes a big difference.”

I hear you knocking: The last time MGM came to the table in January 2021, the bid valued Entain at £8bn or £13.83 a share, which at the time was a 20% premium to the prevailing share price. Now, the shares are trading at £9.27 and the company has a market cap of ~£5.9bn.

“The market may be mispricing Entain right now,” suggested the dealmaker. “But that is the price MGM would have to benchmark its bid against.”

Entain can’t do much about that except try and encourage investors to bid up its share price.

In comparison, any bid for the other half of BetMGM would involve negotiating with management – which knows the long-term value of the business and would price any deal accordingly.

“Logically, it would be much more cost-efficient to acquire all of the parts at a discount than it would be to pay a premium for one of the parts,” the source added.

Whatever you want: For the reasons outlined above, that outcome might be a few months away or more depending on the macro situation. But, all the sources spoken to for this edition agree on the basic premise: the status quo cannot hold for too much longer.

Q3 transactions review

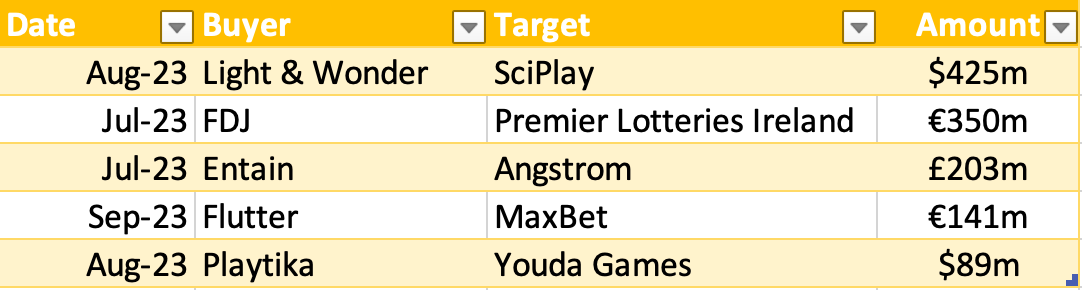

Deals for July-September valued at $1.36bn.

Social interaction: The publicly announced value of the 18 deals noted in the quarter came in at less than half the Q2 amount of $2.8bn. The biggest transaction saw Light & Wonder’s snapping up of the 17% slug of SciPlay that it didn’t already own for $425m, which valued the social gaming business at $2.5bn.

As discussed above, bolt-ons featured once again. FDJ bought Premier Lotteries Ireland for €350m, expanding its European lottery footprint.

Flutter swooped for Serbian operator MaxBet with an initial €141m for a 51% stake.

Meanwhile, Entain bought Angstrom for an initial £81m, rising to £203m depending on contingent payments.

Busy, busy, busy: Of the 18 deals, five were in the affiliate space. One deal saw the continuation of the dismemberment of Catena Media’s European presence with the sale of the Squawka and GG.co.uk brands to Moneta for €6m. The other four all related to Better Collective, as it swooped to buy:

Danish tipster brand Tipsbladet for €6.5m.

Brazilian-facing sports media platform Torcedores.com for an undisclosed sum.

The Swedish-facing sports media brands SvenskaFans.com, Hockeysverige.se, Fotbolldirekt.se and Innebandymagazinet.se from publisher Everysport for €3.7m payable in installments.

Florida-based sports media platform Playmaker HQ for a total of $54m, of which $15m is upfront.

The SKS365 bid battle

Playtech’s brief statement about the news it was involved in the bidding for the company behind the PlanetWin brand suggests others were involved in the bidding.

Incremental: Whoever wins out and gets to augment their standing in Italy with the acquisition of SKS365 will be adding ~10% of the total online betting market to their existing position, according to the analysts at Peel Hunt.

It would be a “useful’ addition for Flutter, the team suggested, and Entain if it didn’t (apparently) have its hands tied by its investors.

For Playtech, meanwhile, a deal at the rumored £500m would be substantial enough to perhaps warrant an equity raise, suggested the team.

They said, on the basis that adding SKS365 would give Snaitech overall market leadership, a deal at this price “would make sense”.

Stand, alone: But, they added, the bolstered market positioning could also prompt further strategic moves. “We believe there is a good argument to be made for demerging Snaitech from Playtech and, if Snaitech had greater scale and synergies to extract, it would make a more appealing standalone prospect for public market investors.”

** SPONSOR’S MESSAGE ** During the Panthers vs Seahawks game that lasted 3 hours and 6 minutes, Huddle had, altogether, 27 minutes and 58 seconds of suspensions, while the market, on average, had 1 hour and 10 minutes of suspension time.

Maintaining top-tier uptime not only enhances the user experience for our clients but also directly contributes to increased customer satisfaction, higher revenue generation, and reducing churn.

Explore more: https://huddle.tech/by-the-numbers-huddles-uptime-performance/

Calendar

Oct 9-12: G2E, Las Vegas

Oct 16: Gaming In Germany, Berlin

Oct 26: Reputation Matters, London

An +More Media publication.

For sponsorship inquiries email scott@andmore.media.